300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

From quality healthcare services to accessing state-of-the-art medical facilities, the Philippines has it all, but with a fraction of the cost back home with health insurance. With that said, navigating the healthcare system in the country is more complex than you might think.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

The Philippines is made up of more than 7,500 islands, and the country has more than 20,000 miles of coastline. Traveling across the country is difficult because there are many remote areas within this geography. Depending on where you are, accessing healthcare could be tricky.

As a result, understanding the world of health insurance in the Philippines, why expats opt for private healthcare, and things you might want to consider when securing international health insurance is essential to preparing yourself for a stress-free stay in the Philippines.

This Pacific Prime article will walk you through all the essential information about health insurance in the Philippines. With all this information in hand, you are guaranteed a worry-free and rewarding experience as an expat in the “Pearl of the Orient Seas”.

Overview of the Healthcare System in the Philippines

The Philippines’ healthcare system is a combination of public and private healthcare. The government funds the public healthcare system through taxes and subsidies, while the private system relies on out-of-pocket payments and private insurance.

Public Healthcare

Public healthcare is composed of government-operated health facilities like community health centers and hospitals, which offer fundamental health services to the general public. This sector of the healthcare system accounts for 40% of all medical facilities in the country.

Private Healthcare

Private healthcare is responsible for the remaining 60% of the healthcare system, comprising privately owned hospitals, clinics, and medical centers offering advanced technology and top-notch facilities.

Government-Sponsored Health Insurance – PhilHealth

PhilHealth is the primary government agency responsible for providing health insurance coverage to Filipinos. It operates under the principle of universal health coverage, aiming to provide all citizens equal access to quality healthcare services in the country.

International citizens who are legal residents in the Philippines are eligible to join PhilHealth. There are two sectors that most expats generally fit into:

- Formal sector: For workers employed by a local business

- Informal Economy: For the self-employed and freelancers

There are four more membership sectors that PhilHealth offers based on the applicant’s work status, income, and age:

- Indigents: For impoverished people subsidized by the national government

- Sponsored members: For people who are subsidized by the national government

- Lifetime members: For retirees and pensioners who previously paid 120 months of premiums

- Senior citizens: For individuals over 60 years of age or older, and do not qualify as lifetime members

For foreigners working in the Philippines, enrolling in PhilHealth is a must. Your employer and you both contribute to the system. This makes you eligible for free healthcare in public facilities across the Phillippines.

The Quality of Healthcare between Urban vs Rural Locations

Healthcare quality generally is lower in rural locations than in urban. There are fewer doctors and nurses, averaging only 1 medical practitioner available for 33,000 rural residents. Specialists are limited in rural areas, and specific treatments for severe conditions are not available.

Fewer doctors and nurses are working in rural areas than in urban areas. There is only 1 medical practitioner available for 33,000 rural residents. Specialists are limited in rural areas, and treatments for some specific conditions like cancer or heart disease are not available.

Public healthcare in the main cities provides excellent care and diagnostic services. This does not apply to all public facilities. That is why those who can afford private health care will opt for it as they are then more likely to access quality care whenever they are in the Philippines.

Although considered adequate and dependable by the local population, there are known issues of long wait times and outdated medical equipment. The issues are consequences of insufficient funding from the government and human resources.

There is a tendency for medical graduates to emigrate to other more developed countries or work in private healthcare establishments for better job opportunities, higher salaries, and a more desirable work environment due to brain drain and economic stagnation in local facilities.

However, one good thing is that medical staff are multilingual. Both public and private hospitals have English-speaking staff so you don’t have to worry about communicating your conditions to staff members.

Why Expats Prefer Private Health Insurance

Generally speaking, public hospitals and other facilities handle preventive and primary care; private facilities on the other hand provide specialized care for complex conditions in addition to what was offered in the public sector, including:

- Preventative medicine

- Diagnostic testing

- Primary care

- Specialist consultations

- Surgical procedures

- Specialized areas of medical care such as dermatology and neurology

Although labeled as expensive according to local standards, private healthcare services are still more affordable than those in Western countries. Therefore, expats in the Philippines prefer accessing healthcare services through the private sector.

Choosing a Private Health Insurance Plan

When choosing a private health insurance plan, some factors to consider are your desired coverage and benefits and more. We will explain the factors to consider in detail below.

Coverage and Benefits

As expats in the Philippines, there are several coverage options that you might want in your international health insurance plan, namely dental and vision, maternity, worldwide coverage, emergency evacuation coverage, and wellness and preventative care.

- Worldwide coverage: Expats may need to travel frequently or require medical treatment outside the Philippines due to medical insufficiency, worldwide coverage ensures that you are protected wherever you go, and access healthcare services back home.

- Maternity coverage: For expat families planning to have children, maternity coverage is imperative for settling hospital bills for prenatal care, childbirth, postnatal care, and hospital stays

- Emergency evacuation coverage: Emergency evacuation coverage plays a vital role in the event of a serious illness or injuries that require specialized treatment not available locally. This coverage ensures that you can be transported to a suitable medical facility or back home for appropriate care.

- Dental and vision coverage: Expats can choose to include dental and vision coverage to cover routine dental check-ups, cleanings, eyeglasses, and contact lenses.

- Wellness and preventative care: This is the coverage for wellness programs, preventative screenings, vaccinations, and health check-ups. This could be useful in the Philippines as the healthcare system largely adopts a prescriptive medicine approach.

Network of Healthcare Providers

International health insurance allows expats to access a large network of medical practitioners and specialists in the Philippines through the private healthcare system. However, the network of healthcare providers solely depends on the connection of your insurance provider.

You should research the clinics and hospitals that are at your convenience to reach and in liaison with your insurer. This ensures that your treatments are covered by health insurance so that you’ll not have to pay anything out-of-pocket.

Premiums, Deductibles, and Copayments

Premiums are the costs of health insurance, which is a concern for many. If you find health insurance suitable for your healthcare needs too expensive, there are two ways you can reduce the premium without fully sacrificing your benefits – deductibles and copayments.

Deductibles are the specific amount you must pay for your medical treatments before your insurance policy pays for the rest of your claims according to the coverage scope and limit of the insurance plan.

Copayments are fixed out-of-pocket amounts paid by the policyholder for a covered healthcare service after the deductible has been paid. Splitting the cost of medical services between the insurance provider and the policyholder keeps your monthly medical bills in check.

Navigating the Process of Health Insurance

Securing comprehensive health insurance in the Philippines for your needs requires a series of processes – researching and comparing health insurance options, understanding the enrollment process, making informed decisions about coverage and benefits, and managing claims.

1. Researching and comparing Health Insurance Options

Start by identifying your specific healthcare needs and priorities, and consider factors such as your age, medical history, family size, and budget. These factors will influence your premium to be paid and coverage selection.

Once you have an idea of your health priorities, research different health insurance providers who offer coverage in the Philippines. It is advisable to check out reputable companies as they are more financially stable and with a long history of positive customer reviews.

To help you lock in a list of preferred insurance providers, you can check out their network of healthcare providers. Make sure that there are hospitals, clinics, and doctors nearby so that you can access healthcare services whenever needed.

Consider Working With an Insurance Broker

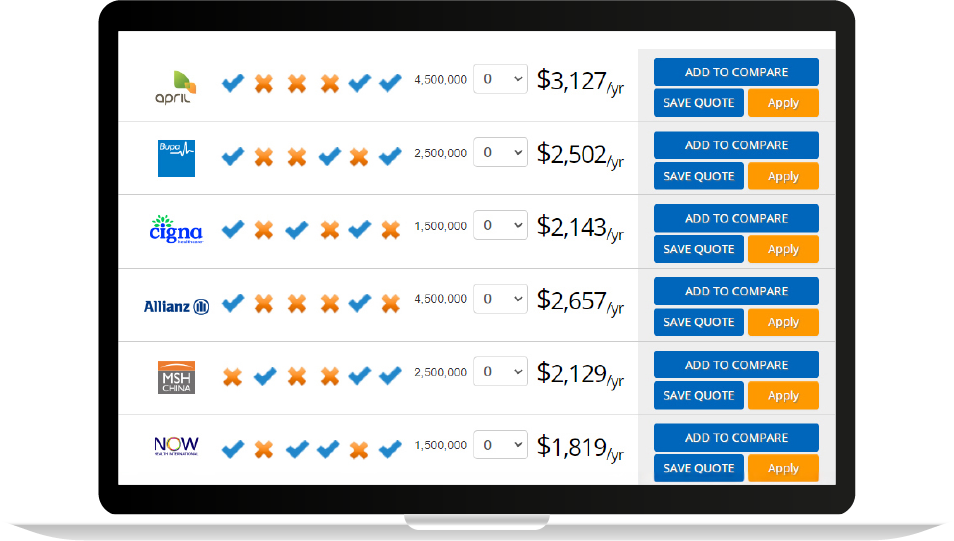

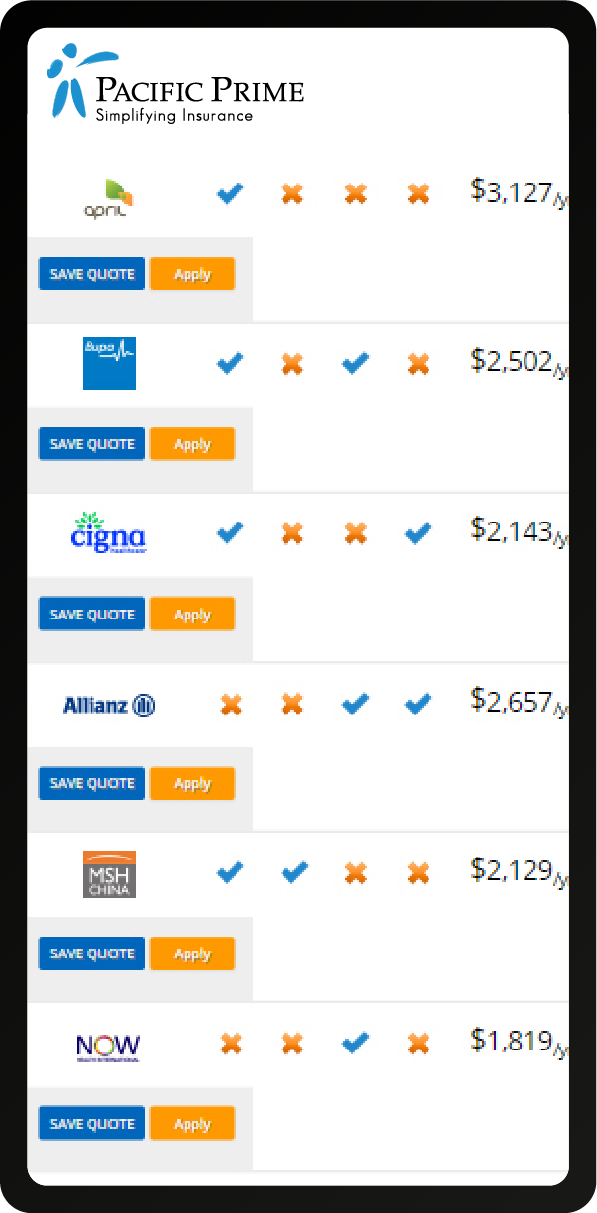

By working with a reputable global-scale insurance broker like Pacific Prime, you have all the extra value-added services that you may not receive by reaching an insurance provider directly, with no additional costs.

Our team of expert insurance advisors is here to talk through your needs and give you an obligation-free comparison quote so that you know whether the plan you are considering is in alignment with your requirements and budget.

Note: You can also make use of our online quote tool to generate a quote by yourself. Check out our tutorial on how to use it.

2. Understanding the Enrollment Process

Each health insurance policy has different eligibility, based on factors such as your age, employment status, and income level.

Make sure you have documents for enrollment readied, including identity proof, medical history, and employment records.

Follow the necessary steps according to the health insurance provider and complete the enrollment process.

3. Making Informed Decisions about Coverage and Benefits

Before signing the policy, carefully review the terms and conditions of the policy. Remember to find out all the coverage limits, exclusions, and waiting periods for individual items by reading the fine print.

Note: Should you have any questions or concerns regarding your policy, ask the insurance provider or the insurance broker you are working with for clarification.

4. Managing Health Insurance Claims

It’s essential to familiarize yourself with the claims process for your health insurance plan. Understand the required documentation and procedures for submitting a claim so you can be better prepared for things you’ll need for a successful claim.

In the Philippines, it is quite common for hospitals to charge you upfront then you’ll be reimbursed by your insurance provider once the claim goes through. However, this varies among insurers so it might be best to get confirmation from yours.

If you happen to have a denied claim, review the reason provided by your insurer. Consider filing an appeal if you believe it is justified. Your insurance broker will help negotiate with the insurance provider as well.

Frequently Asked Questions

What is the difference between government-sponsored health insurance and private health insurance options in the Philippines?

Government-sponsored health insurance programs, like PhilHealth, are funded by the government and provide coverage to eligible individuals. Private health insurance options, on the other hand, are offered by private companies and often provide more comprehensive coverage but require premiums.

How do I enroll in a health insurance plan in the Philippines?

To enroll in a health insurance plan in the Philippines, you need to meet the eligibility requirements and complete the enrollment process. For PhilHealth, you can enroll online or visit their offices; private health insurance enrollment can be done online, through agents, or at their offices.

What factors should I consider when choosing a health insurance plan in the Philippines?

When choosing a health insurance plan in the Philippines, consider factors such as coverage for hospitalization, outpatient services, and pre-existing conditions. Compare premiums, co-payments, deductibles, and the network of healthcare providers to ensure they align with your needs and budget.

Conclusion

Through understanding the healthcare system in the Philippines, you’ll be equipped with the necessary information and knowledge to make informed decisions on whether to enroll in international private health insurance.

Pacific Prime has over 20 years of experience in helping expats secure the best international health insurance for their requirements and budget. Our team of insurance specialists is trained to compare and choose a policy from globally renowned insurance providers, and offer value-added services.

Contact us today for impartial advice and an obligation-free quote, and have us protect your safety during your journey in the Philippines!

Since joining Pacific Prime, Eric was exposed to a new world of insurance. Having learned about insurance products extensively, he has taken joy and satisfaction in helping individuals and businesses manage risks and protect themselves against financial loss through the power of words.

Although born and raised in Hong Kong, he spent a quarter of his life living and studying in the UK. He believes his multicultural experience is a great asset in understanding the needs and wants of expats and globe-trotters.

Eric’s strengths lie in his strong research, analytical, and communication skills, obtained through his BA in Linguistics from the University of York and MSc in Teaching English to Speakers of Other Languages (TESOL) from the University of Bristol.

Outside of work, he enjoys some me-time gaming and reading on his own, occasionally going absolutely mental on a night out with friends.

- Dubai Laws for Expats: Key Rules to Know Before Moving – October 17, 2025

- Cost of Living in Japan for Expats: Housing, Visas & Tips – October 14, 2025

- Cost of Giving Birth in Mexico: Expenses, Care, and Benefits – August 19, 2025