300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Exclusions in insurance refers to events, situations, and causes that would prevent a policy from covering you. Individuals in Singapore picking an insurance plan will want to understand their private health insurance plan exclusions so they don’t risk paying any unexpected medical expenses.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Do you know what are the common exclusions in the world of insurance? Do you know how you can mitigate the risk of paying excluded services out of pocket?

This Pacific Prime article walks you through the most typical exclusions that apply to private health insurance plans so that you are aware of the insurance coverage when searching for the right plan for your needs among insurers in Singapore.

What Are Exclusions?

Exclusions in health insurance refer to conditions, situations, or events outside coverage under a policy. Medical expenses associated with excluded treatments are not eligible for reimbursement nor are they subjected to direct billing. One must pay out-of-pocket to settle the medical bill.

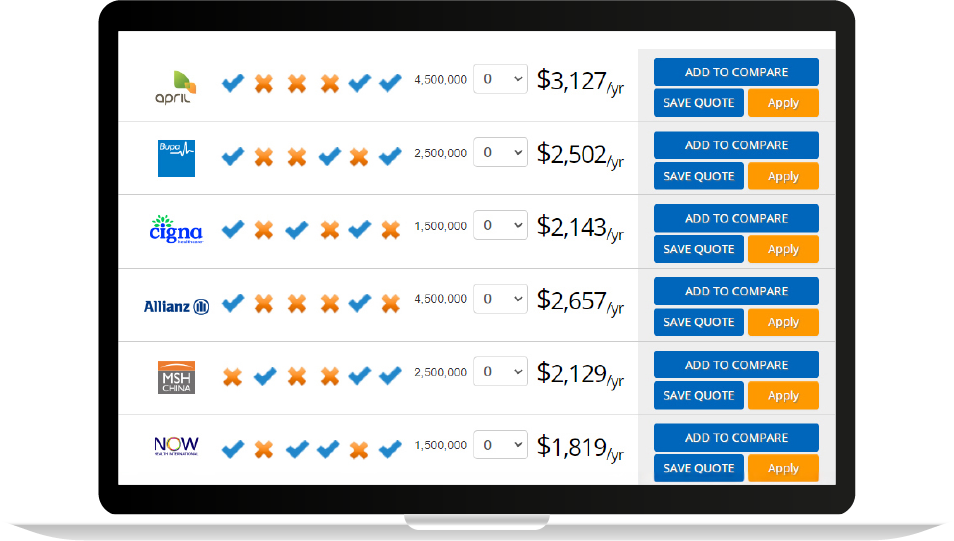

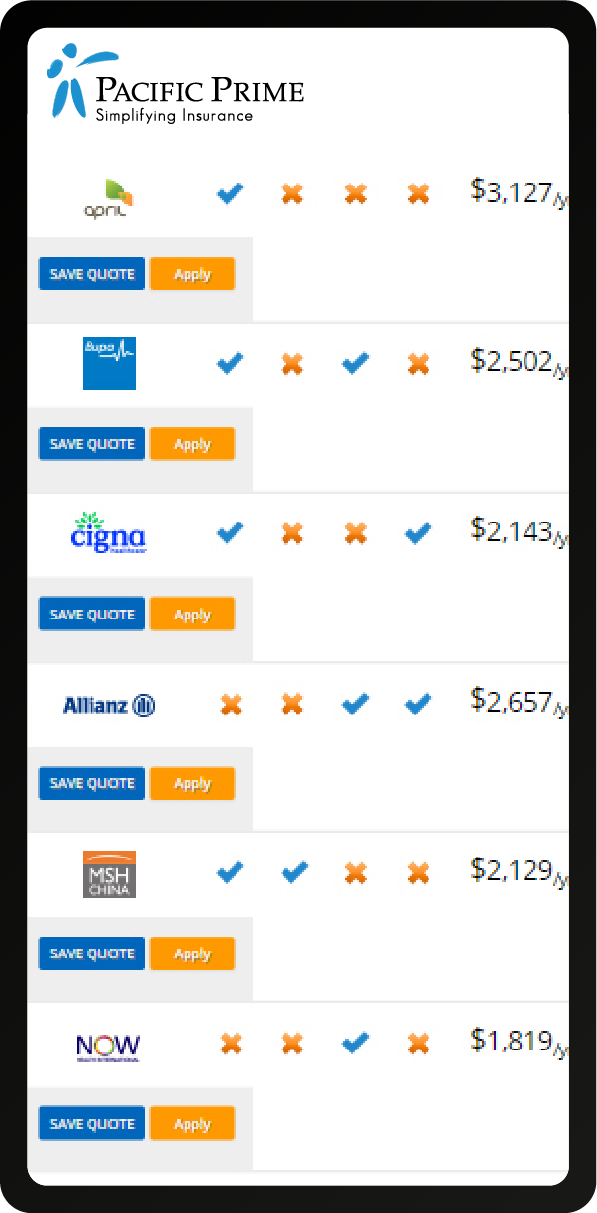

It is worth noting that every health insurance policy has exclusions, and they vary among insurers. Therefore, you are advised to compare policies in the market and check the fine print before settling on a desired health insurance plan.

Here are some items that are most typically excluded from coverage in health insurance policies. Some of the exclusions can be covered depending on the decision of the insurer, but usually under stated conditions.

Exclusions: Pre-existing / Chronic Medical Conditions

Some insurance plans also exclude chronic conditions, referring to medical conditions that require long-term monitoring, are likely to recur, or have no known cure. Some examples are asthma, arthritis, and diabetes.

A pre-existing condition is an injury or illness that you currently have or previously had before enrolling in your health insurance policy. Common examples include heart disease, cancer, and AIDS.

You will be asked to declare any pre-existing medical conditions. It is important to be transparent and truthful with your medical history as failure to do so is regarded as non-disclosure which could invalidate your insurance coverage.

The outcomes of an underwriting assessment with pre-existing conditions could be as follows:

- Coverage on a Moratorium Basis: This means your pre-existing condition can be covered, but only once you’ve been free from medication, treatment, diagnostic tests, or advice for the condition for two continuous years after your coverage started.

- Coverage at a Higher Premium: This allows your pre-existing condition to be covered at the cost of a high premium, as the insurer will need to factor in the risk of your pre-existing condition.

- No Coverage: Your pre-existing conditions might simply be excluded from coverage.

Exclusions: Ancillary Hospital Charges

Ancillary hospital charges are charges from a hospital that are not considered medically necessary. You might be subjected to paying out-of-pocket for miscellaneous charges such as guest meals, telephone calls, extra pillows, and the use of TV.

In-patient benefits of a health insurance plan usually address the most core aspects of hospital charges such as surgery, ambulance, room and board fees, lab tests, and anesthetist charges. These are considered medically necessary charges during your stay at the hospital.

Exclusions: Specific Scenarios

In certain specific scenarios, most health insurance plans will not provide coverage. Commonly excluded scenarios include:

- Injuries or illnesses caused by hazardous use of alcohol or drugs

- Injuries or illnesses caused by participation in criminal activities

- Injuries or illnesses sustained as a direct result of a natural disaster

- Self-inflicted injuries

- Treatments arising from war or terrorist acts

- Injuries sustained from engaging in professional sports

Exclusions: Cosmetic Surgery

Health Insurance plans only cover treatments that are deemed medically necessary so cosmetic surgeries are not covered as they are considered a matter of personal choices. Hence, surgeries for aesthetic purposes such as facelifts and rhinoplasties are not covered.

In some exceptional cases, you might be able to reclaim the costs of certain cosmetic treatments such as facial reconstruction after an accident. This, however, is an unlikely case for most people going for cosmetic surgery.

Exclusions: Treatments Outside Singapore

Local health insurance plans usually do not provide coverage and benefits outside of Singapore. As expats, you might need to travel frequently (with your family). If that’s the case, then taking out an international health insurance plan would be the best option.

International health insurance will offer coverage at almost any hospital, anywhere in the world. You can rest assured that you receive world-class healthcare services in top-notch private medical facilities, without having to worry about financial issues and long wait times.

Understanding Policy Exclusions

To navigate insurance exclusions effectively, policyholders should take certain steps to ensure clarity and understanding:

- Thoroughly Read Policy Documents

- Consult with Insurance Brokers or Professionals

- Seek Clarification on Specific Exclusions

Thoroughly Read Policy Documents

It is essential to carefully review the entire insurance policy, including the terms, conditions, and exclusions, before purchasing insurance. Policyholders should pay close attention to the exclusion section to identify any potential limitations or restrictions on coverage.

Consult with Insurance Brokers or Professionals

Seeking guidance from experienced insurance brokers or agents can be immensely helpful. These professionals have in-depth knowledge of insurance policies and can provide valuable insights and clarifications regarding specific exclusions.

Through consultation with them, policyholders can better understand the implications of exclusions and advise on suitable coverage options that align with their needs and risk tolerance.

Seek Clarification on Specific Exclusions

If there are any doubts or uncertainties about specific exclusions, it is advisable to contact the insurance provider or broker directly. They can clarify the extent of coverage and any potential gray areas.

It is crucial to obtain written or documented clarification to ensure clarity and avoid misunderstandings in the future.

Mitigating Exclusion Risks

Understanding policy exclusions and taking appropriate measures to mitigate them allows individuals in Singapore to secure insurance protection that aligns with their needs while avoiding potential pitfalls.

Policyholders can navigate exclusions in insurance policies more effectively, minimize risks, and make informed decisions by following the guidelines below.

Seeking Additional Coverage or Riders

When certain exclusions pose significant risks, policyholders can explore additional coverage options or riders. These additional provisions can help address specific exclusions and provide extended coverage. For example, in health insurance, policyholders may opt for a rider that covers pre-existing conditions, offering protection for medical conditions that existed before obtaining the insurance.

Exploring Different Insurance Providers

Comparing policies from multiple insurance providers allows individuals to evaluate coverage options and find the best fit for their needs. Different providers may have varying exclusions and inclusions in their policies.

By conducting thorough research and obtaining quotes from various insurers, policyholders can identify policies that offer broader coverage and minimize the impact of exclusions.

Maintaining Accurate and Updated Information

Accurate and updated information is crucial when purchasing and maintaining insurance coverage. Policyholders should provide complete and precise information about their health, property, or any other relevant aspects during the application process.

Failing to disclose crucial information may lead to exclusions or denial of claims. Regularly reviewing and updating policy details is also important to ensure that coverage remains relevant and adequate over time.

Complying with Policy Terms and Conditions

Adhering to the terms and conditions outlined in the insurance policy is vital. Failure to comply with policy requirements, safety guidelines, or any other stipulations may result in exclusions or claim denials.

Policyholders should familiarize themselves with the obligations mentioned in the policy and ensure they meet them to maintain the validity of their coverage.

Frequently Asked Questions

What are insurance exclusions?

Insurance exclusions refer to specific situations, conditions, or events that are not covered by an insurance policy. These exclusions are typically outlined in the policy document and can vary depending on the insurance provider.

What are some common exclusions in insurance policies?

The specific exclusions in insurance policies can vary widely, and it is essential to review the policy document carefully. However, there are some common exclusions in various types of insurance policies in Singapore. For example, pre-existing conditions and cosmetic treatments.

How do insurance exclusions affect claims?

Insurance exclusions directly impact the coverage provided by an insurance policy. If an event or circumstance falls under an exclusion listed in the policy, the insurance company will not be obligated to provide coverage.

Can insurance exclusions be modified or removed?

Insurance exclusions are typically determined by the insurance company and are part of the contractual agreement. But, whether it can be modified or removed depends on the specific terms and conditions of the insurance policy and the willingness of the insurance company.

Conclusion

By knowing the common exclusions of health insurance, you are now equipped to make informed decisions on whether the health insurance policy is on par with what you need to stay physically and mentally healthy in Singapore.

Pacific Prime is an award-winning insurance brokerage with over 20 years of experience in the industry. We leverage our connection with global insurers to help you search for an insurance plan that is compatible with your medical needs and budgets.

Contact us today for a piece of impartial advice from our team of insurance experts, or get an obligation-free quote!

Enjoyed the read? If you would like to learn more about outpatient benefits and waiting periods for dental benefits in Singapore, look no further than here!

Since joining Pacific Prime, Eric was exposed to a new world of insurance. Having learned about insurance products extensively, he has taken joy and satisfaction in helping individuals and businesses manage risks and protect themselves against financial loss through the power of words.

Although born and raised in Hong Kong, he spent a quarter of his life living and studying in the UK. He believes his multicultural experience is a great asset in understanding the needs and wants of expats and globe-trotters.

Eric’s strengths lie in his strong research, analytical, and communication skills, obtained through his BA in Linguistics from the University of York and MSc in Teaching English to Speakers of Other Languages (TESOL) from the University of Bristol.

Outside of work, he enjoys some me-time gaming and reading on his own, occasionally going absolutely mental on a night out with friends.

- Dubai Laws for Expats: Key Rules to Know Before Moving – October 17, 2025

- Cost of Living in Japan for Expats: Housing, Visas & Tips – October 14, 2025

- Cost of Giving Birth in Mexico: Expenses, Care, and Benefits – August 19, 2025