300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

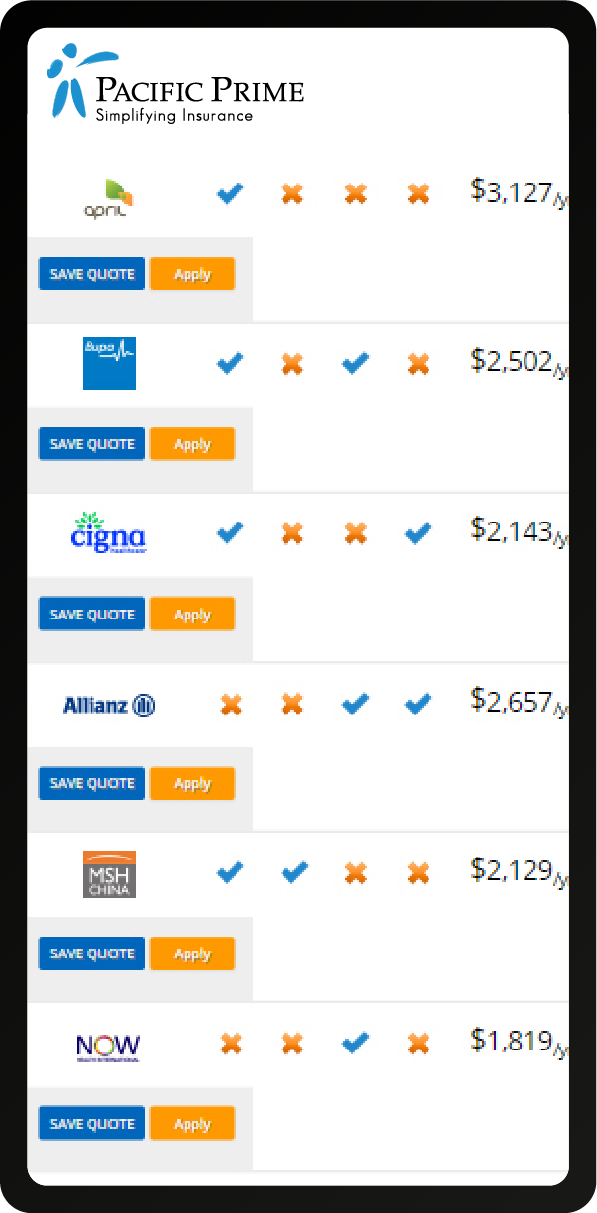

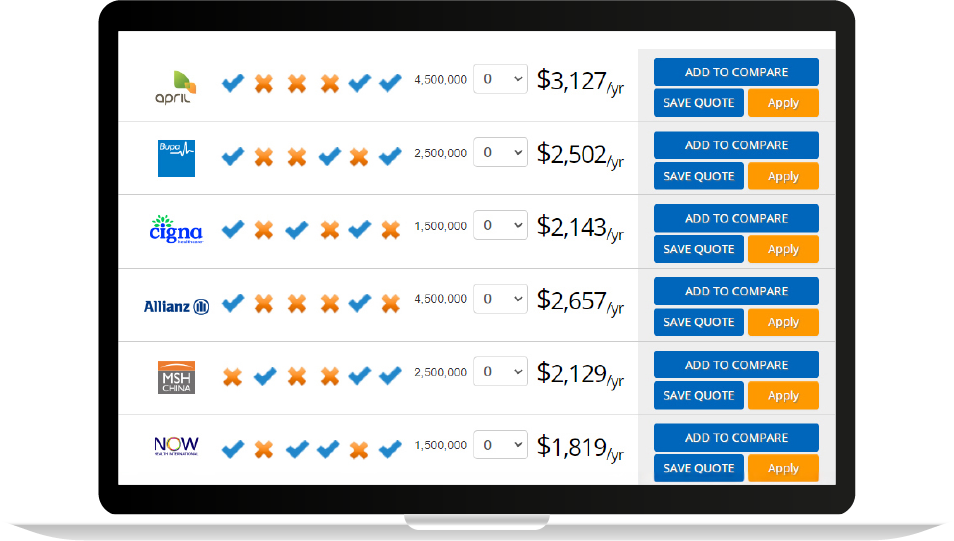

Leading providers like Bupa Global, Allianz Care, and Cigna Global are among the best for those with type 2 diabetes, offering flexible plans, strong networks, and benefits that support ongoing treatment—helping expats access quality care worldwide.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Living abroad with type 2 diabetes brings unique challenges, from accessing medication to navigating insurance rules. This guide helps expats understand coverage, compare top global insurers, and choose a plan that supports ongoing care anywhere in the world.

What is Type 2 Diabetes?

Type 2 diabetes is a long-term condition where the body either resists insulin or doesn’t produce enough. This leads to high blood sugar levels. It typically develops in adults and is often associated with lifestyle and metabolic factors.

Type 1 vs. Type 2 Diabetes

Type 1 diabetes is caused by the immune system attacking insulin-producing cells. It usually begins in childhood. Type 2 is more common, develops later, and is often tied to diet, weight, and activity levels.

Why It’s a Serious Health Concern

Uncontrolled Type 2 diabetes can lead to heart disease, kidney failure, nerve damage, and vision loss. These complications can be life-threatening and often worsen silently over time without proper management.

Causes, Risks & Prevention

Risk factors include obesity, inactivity, poor diet, and genetics. Prevention focuses on healthy eating, regular exercise, weight control, and routine checkups. Early lifestyle changes can delay or even prevent the onset.

How Type 2 Diabetes Affects Health Insurance

Type 2 Diabetes can lead to higher insurance premiums, limited coverage, or exclusions. If you’re at risk, insurers may be cautious. If diagnosed, it’s considered a pre-existing condition, and some providers may not cover related medical expenses.

Type 2 Diabetes as a Pre-existing Condition

Insurers classify Type 2 diabetes using factors such as age at diagnosis, treatment type, blood sugar control, and any complications. Strong blood sugar management and fewer complications can improve your insurance standing and may unlock better coverage terms.

Many insurers impose a waiting period of up to one year for diabetes-related claims. During this time, doctors’ visits, medication, and tests for Type 2 diabetes may not be covered. Always check your policy’s fine print to understand any specific waiting periods.

Impact on Premiums

Type 2 diabetes can increase your health insurance costs. Carriers consider the extra risk and adjust premiums to cover expected medical needs. Understanding this impact helps you plan your budget and compare policies with similar rate structures.

Insurers assess several factors: how severe your diabetes is, how well you control your blood sugar, any related complications like heart or kidney issues, and your overall health profile. Better health markers usually mean smaller premium increases.

While premiums will increase for individuals with type 2 diabetes, they can still limit the increase through healthy lifestyle habits. Effective management through diet, exercise, and medication can limit the increase. Insurers may reward consistent control with more favorable rates.

Maintaining stable blood sugar shows insurers you’re managing your condition well. This can lead to smaller premium hikes or even discounts. Regular monitoring, follow-up tests, and meeting target glucose goals demonstrate lower risk and improve your rate of outcome.

Coverage for Cholesterol Management

- Routine doctor visits (PCP, endocrinologist, ophthalmologist, podiatrist)

- Diabetes self-management education (DSME) programs

- Prescription medications (e.g., oral medications, insulin, and other injectable medications)

- Supplies for Type 2 Diabetes patient (e.g., Blood glucose monitors and test strips, Insulin pens, syringes, and pumps, Continuous Glucose Monitors (CGMs))

- Diagnostic tests (e.g., A1C tests, lipid panels, kidney function tests, eye exams (retinopathy screenings), and foot exams)

- Complications management (e.g., coverage for treatment of neuropathy, nephropathy, retinopathy, and cardiovascular issues, specialized wound care)

- Specialist consultations (e.g., cardiologists, endocrinologists)

- Lifestyle intervention programs

Navigating Health Insurance with Type 2 Diabetes

For those with type 2 diabetes, it is easier to have the condition covered by health insurance when compared to type 1 because it is more manageable without medication.

Choosing the Right Plan for Chronic Disease Management (e.g., PPO, HMO, HDHP)

Look at plan types like PPO, HMO, and HDHP. PPOs offer flexible provider access; HMOs focus on cost and referrals; HDHPs pair lower premiums with high deductibles and HSA options. Match plan rules to your treatment needs and budget.

Importance of Accurate Disclosure During Enrollment

When enrolling for your selected plan, it is crucial that you provide full details of your type 2 diabetes diagnosis and treatment history to prevent future claim denials. Keep medical records and test results ready to verify your condition and ensure proper coverage.

Understanding Your Plan’s Formulary for Type 2 Diabetes Medications and Supplies

Check your plan’s drug formulary for covered diabetes medications and supplies such as insulin, test strips, and pumps. Note tier levels, copay amounts, and any restrictions. Ask about updates each year and explore cost-assistance or mail-order options.

Prior Authorization Requirements for Specific Drugs, Devices, or Procedures

Some diabetes treatments need insurance approval before you can get them. This is called ‘prior authorization’, and it applies to certain drugs, devices, or medical procedures.

Your doctor must send details to your insurer explaining why the treatment is needed. Without this step, coverage may be delayed or denied. Planning ahead with your healthcare team is crucial to prevent treatment gaps.

Below are common type 2 diabetes treatments that often require prior authorization:

- GLP-1 receptor agonists like Ozempic, Trulicity, and Victoza

- Newer insulins such as Toujeo or Tresiba

- Continuous Glucose Monitors (CGMs) like Dexcom G7 or FreeStyle Libre

- Insulin pumps and related pump supplies

- Combination drugs like Mounjaro (tirzepatide)

Strategies For Appealing Denied Claims Related to Diabetes Care

Insurance denials for diabetes care can be overturned with the right approach. By understanding the reason, gathering strong medical evidence, meeting deadlines, and staying organized, you can improve your chances of getting the coverage you need.

If your insurance denies a diabetes-related claim, start by carefully reading the denial letter. It explains the reason and outlines the appeal process.

Gather supporting documents, such as medical records, prescriptions, and letters from your doctor explaining why the treatment is necessary.

Submit your appeal within the stated deadline. Missing it can mean losing your right to challenge the decision. Be sure to follow up regularly with your insurer to track progress. Keep records of all calls, emails, and letters for reference.

Quick Checklist

- Read the denial letter to understand the reason and appeal steps

- Collect medical evidence like records, prescriptions, and doctors’ notes

- Submit before the deadline stated in the letter

- Follow up regularly with your insurer

- Keep a log of all calls, emails, and letters

Best Health Insurance for Type 2 Diabetes

Managing type 2 diabetes abroad means needing reliable coverage, global care access, and benefits for ongoing treatment. Bupa Global, Allianz Care, and Cigna Global offer flexible plans, strong networks, and support for expats worldwide.

Allianz Care

Allianz Care is a top global insurer for expats, offering health, life, critical illness, and disability coverage. Its three flexible plans—Care, Care Plus, and Care Pro—serve students, nomads, expats, and expat families.

Each plan can be further enhanced with optional add-ons, including Outpatient, Dental, and Repatriation Plans. Allianz’s global reach, tailored benefits, and strong support make it easier for people with type 2 diabetes to access quality care wherever they live.

| Allianz Care Expat Health Insurance Plans Comparison (USD) | |||

| Benefits Coverage | Care Plan | Care Plus Plan | Care Pro Plan |

| Maximum Plan Limit | $2,500,000 | $4,000,000 | $5,000,000 |

| Type of Room | Semi-Private | Private | Private |

| Inpatient / Day-Care | ✓ | ✓ | ✓ |

| Medical Evacuation | ✓ | ✓ | ✓ |

| Rehabilitation Treatment | $2,700 | $3,375 | $5,970 |

| Preventive Surgery | ✗ | ✗ | $40,500 |

| Emergency Out-Patient Treatment | $338 | $1,015 | $1,015 |

| Olive Health & Wellness Support Program | ✓ | ✓ | ✓ |

| Second Medical Opinion Service | ✓ | ✓ | ✓ |

Bupa

Bupa Global offers plans from major medical coverage to comprehensive options with wellness exams—ideal for ongoing diabetes care. Its global network, direct billing, and 24/7 Global Virtual Care make it easy to access treatment anywhere in the world.

Patients can see specialists without referrals and get second opinions, ensuring informed decisions for complex conditions.

Benefits include lifetime renewal, private hospital rooms, and coverage for two children under 10 at no extra cost (subject to underwriting). Bupa’s MembersWorld online and app tools, plus a worldwide provider search, help manage care and find trusted facilities with ease.

| Annual Benefit Limits of Bupa Global Health Plans | ||

| Plan | Annual Benefit Limit GBP | Annual Benefit Limit USD |

| Major Medical | £2,500,000 | About $3,174,200 |

| Select | £1,250,000 | About $1,587,100 |

| Premier | £1,875,000 | About $2,380,600 |

| Elite | £3,750,000 | About $4,761,300 |

Cigna

Cigna Global offers Silver, Gold, and Platinum international health plans in over 200 markets, with 1.5 million health professionals and 24/7 multilingual support for individuals, families, and businesses.

These plans offer worldwide coverage, inpatient and mental health care, cancer care, and private rooms—vital for managing diabetes. With limits from USD $1 million to unlimited, Cigna delivers flexible, reliable protection worldwide.

Other features include global health assistance, visitor accommodation costs, multiple deductible options, and an easy-to-use online platform.

| Cigna Health Insurance Plans: Standard Medical Benefits (USD) | ||||

| Coverage Benefits | Silver | Gold | Platinum | Close Care |

| Annual Limit Amount | $1,000,000 | $2,000,000 | Unlimited | $500,000 |

| Coverage Area | Worldwide | Worldwide | Worldwide | Country of residence |

| Inpatient and Daypatient Treatment | Paid in full for a private room | Paid in full for a private room | Paid in full for a private room | Paid in full for a semi-private room |

| Hospital Accommodation for Parent or Guardian | $1,000 | $1,000 | Paid in full | Not Covered |

| Inpatient Cash Benefit | $100 | $100 | $100 | $100 |

| Transplant Services | Paid in full | Paid in full | Paid in full | Not Covered |

| Rehabilitation | $5,000 | $10,000 | Paid in full | $2,000 |

| Prosthetic Devices | Paid in full | Paid in full | Paid in full | Internal devices are paid in full; external devices are up to $2,500 |

| Ambulance Services | Paid in full | Paid in full | Paid in full | Paid in full (road only) |

| Treatment for Obesity | Not Covered | 70% refund up to $20,000 | 80% refund up to $25,000 | Not Covered |

| Congenital Conditions | $5,000 | $20,000 | $39,000 | Not Covered |

Frequently Asked Questions

Does insurance cover all my diabetes medications and supplies?

Most plans cover insulin, oral medications, test strips, and devices, but coverage levels, copays, and formularies vary. Always check your plan’s drug list.

Are continuous glucose monitors (CGMs) and insulin pumps covered?

Treatments like CGMs and insulin pumps may be covered if they are deemed medically necessary, but prior authorization is often required. To ensure that they are covered by your plan, it is vital that you work with your doctors and plan ahead to have them authorized.

What should I do if my claim for diabetes care is denied?

Review the denial letter, gather medical evidence, and file an appeal within the stated deadline. It is crucial to regularly follow up with your insurer after you have submitted your appeal.

Conclusion

For expats with type 2 diabetes, the right insurance ensures access to quality care abroad. Knowing coverage rules, prior authorizations, and appeal steps helps avoid costly gaps.

Top providers like Bupa Global, Allianz Care, and Cigna Global offer flexible plans, strong networks, and benefits for ongoing treatment worldwide. Choosing the right plan can be daunting—Pacific Prime helps simplify the process.

Pacific Prime is a global insurance broker with over 25 years of experience in the insurance industry. Our insurance experts can help you filter through different insurance plans from our extensive list of insurance partners to help you find a plan that suits you.

Contact us today for impartial advice or an obligation-free quote!

Disclaimer: If you are diagnosed with type 2 diabetes before enrolling in a health insurance plan, the insurer may review your application through medical underwriting. This means coverage, premiums, or eligibility could be based on your current health condition.

Born and raised in the cultural melting pot that is Hong Kong, and having studied at an international school, Vista has developed a multicultural perspective that he uses in his writing and strives to connect to people of different backgrounds.

In his free time, Vista enjoys immersing himself in different worlds, from video games to light novels and movies. His hobbies help him expand his writing style by putting himself in the point-of-view of different people and characters.

- Best International Health Insurance Plans for Expats in Fiji – October 17, 2025

- Best International Health Insurance Plans for Expats in Kosovo – October 17, 2025

- How to Get UAE Citizenship in Dubai – October 17, 2025