300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Minor back pain is one of the most common health issues expats face, yet many are unsure how it’s handled by health insurers. From how insurers assess pre-existing conditions to whether physiotherapy, medication, or specialist consultations are included, coverage can vary widely.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

In this Pacific Prime article, we break down what expats need to know about health insurance and minor back pain, along with practical tips for selecting a plan that provides the right level of support abroad.

Note: If you already have minor back pain before joining a plan, the insurer will evaluate your coverage based on your current health condition through a process called medical underwriting. Exclusions, waiting periods, or premium adjustments may apply depending on the insurer’s assessment.

Understanding Minor Back Pain

Minor back pain refers to mild, short-term discomfort in the back. Unlike chronic or severe back pain, which can last for months and significantly affect mobility, minor back pain tends to be temporary and doesn’t usually require urgent medical care.

Common Causes

For many expats, everyday factors can trigger minor back pain. Muscle strain from lifting luggage or moving furniture, long hours of sitting with poor posture, or even minor sprains from exercise are frequent culprits.

Simple lifestyle adjustments like setting up an ergonomic workstation or stretching regularly often make a noticeable difference.

Typical Symptoms

Minor back pain often shows up as a dull ache, stiffness, or soreness in a specific area of the back. Unlike chronic conditions, the discomfort usually doesn’t radiate down the legs or cause significant weakness.

Most people notice mild back pain after certain activities like sitting for long periods, lifting heavy items, or sleeping in awkward positions, and it generally eases with rest, gentle movement, or over-the-counter medicines.

Why Addressing Minor Back Pain is Important

If left untreated, minor back pain can gradually develop into more persistent or even chronic problems, such as:

- Chronic back pain: Repeated strain without proper rest, stretching, or treatment can turn short-term discomfort into long-lasting pain that’s harder to manage.

- Reduced mobility and flexibility: Ignoring stiffness can make it harder to move freely, affecting everyday activities like sitting, walking, or exercising.

- Muscle imbalances: Pain often causes people to adjust their posture or movement to “protect” the sore area, which may create new strains in other muscles over time.

- Increased risk of injury: Weak or tight muscles from ongoing discomfort can make the back more vulnerable to sprains or disc problems.

- Impact on quality of life: Even mild but recurring pain can affect sleep, productivity at work, and overall wellbeing.

By managing pain early through healthy posture, stretching, and timely medical advice when needed, expats can maintain their mobility, comfort, and overall quality of life while adjusting to a new environment.

How Minor Back Pain Affects Health Insurance

“Minor back pain” usually falls under musculoskeletal conditions. If you’ve had symptoms before your new policy starts, most international insurers treat it as a pre-existing condition, which can affect what’s covered and how much you pay.

Definitions of pre-existing conditions are fairly consistent across international health plans: any illness or symptom that existed before the policy start date may be limited, excluded, or require a waiting period.

Understanding Pre-Existing Conditions

Back pain is extremely common and often short-lived, but prior episodes still count as pre-existing for underwriting purposes. Expect insurers to look at your symptom history, recent treatment (e.g., physio, analgesics), investigations (X-ray/MRI), and any time off work.

These factors will determine whether back-pain-related care is covered right away, covered with limits, or excluded.

Underwriting Approaches

When insurers handle minor back pain, they will use two common types of medical underwriting: full medical underwriting and moratorium underwriting.

Full Medical Underwriting (FMU)

With full medical underwriting, you provide your complete medical history when applying for an international health insurance plan. The insurer reviews your past and current conditions in detail before issuing the policy. Based on their risk assessment, they may:

- Accept you on standard terms (full coverage)

- Accept you, but exclude certain conditions

- Accept you with higher premiums or special terms

- Decline your application if the risk is too high

The advantage of FMU is certainty: you know upfront what is and isn’t covered before the policy starts.

Moratorium Underwriting

With moratorium underwriting, you don’t need to disclose your full medical history at the start. Instead, pre-existing conditions are automatically excluded for a waiting period, usually around 24 months.

If you stay symptom-free and don’t need treatment during that time, the condition may become eligible for coverage afterward.

The benefit of a moratorium is simplicity when applying, but the downside is uncertainty: claims related to your past conditions may be assessed later, at the time of claim, which can sometimes delay payouts.

Impact on Health Insurance Premiums

When it comes to minor back pain, the way insurers assess your medical history will influence how much you pay for coverage.

Several factors typically come into play, such as how often you’ve experienced back pain in the past, how long each episode lasted, what types of treatment you sought (e.g., physiotherapy, imaging, or medication), and whether your back pain is linked to other conditions.

For many expats, a one-off episode of minor back pain that resolved quickly may have little to no effect on premiums. However, if your medical history shows recurring or persistent back pain, even if it’s not classified as severe, insurers may view it as a higher risk.

Example: Imagine two expats applying for international health insurance. The first experienced a sore back after a long-haul flight, rested for a week, and hasn’t had any issues since. Their insurer is unlikely to impose restrictions, as the episode was minor and isolated.

The second expat, however, reports mild but recurring back pain that requires regular physiotherapy sessions. Even though the condition isn’t severe, the insurer may apply a premium loading or exclude future back-related claims to account for the higher likelihood of ongoing treatment.

In such cases, you might face a rise in your premium rates or specific exclusions related to musculoskeletal care. Being transparent about your history helps ensure that your coverage terms are clear from the start and prevents issues at claim time.

Coverage for Minor Back Pain Management on Expat Insurance

Coverage for minor back pain management varies between insurers and policies, but comprehensive international health insurance usually includes a wide range of services, from consultations and prescription medications to physiotherapy, diagnostics, and, in rare cases, surgery if medically necessary.

Coverage for minor back pain management may include:

Doctor Consultations

Most international health insurance plans cover doctor visits related to back pain. This typically starts with a general practitioner (GP) consultation, where you’ll receive an initial assessment and, if needed, a referral to a specialist.

Medications

Over-the-counter pain relievers such as paracetamol or ibuprofen are usually not reimbursed and need to be paid out of pocket. However, prescription medications, such as stronger NSAIDs or muscle relaxants, may be covered if prescribed by a licensed doctor.

Coverage levels depend on the plan’s drug formulary and may include cost-sharing, co-pays, or limits on certain categories of medication.

Physical Therapy and Rehabilitation

Some expat health plans may provide coverage for physiotherapy, chiropractic care, or osteopathy sessions, as these are common treatments for minor back pain.

However, insurers often place limits on the number of sessions per year, require a GP or specialist referral, or cap the maximum reimbursement. Expats should check their policy’s outpatient benefits section to understand the scope of coverage and any restrictions.

Diagnostic Procedures

For minor back pain, diagnostic imaging such as X-rays is less common but may be covered if deemed medically necessary. More advanced imaging, like MRI or CT scans, is typically only approved when symptoms persist or suggest something more serious.

In such cases, most insurers usually require prior authorization and strong medical justification to cover the costs, as these procedures are significantly more expensive.

Other Therapies

Complementary approaches, such as massage therapy or acupuncture, are generally not included in standard international health insurance policies. Expats interested in these therapies should consider purchasing supplementary wellness or alternative treatment benefits if available.

Navigating Health Insurance for Expats with Minor Back Pain

As an expat managing a pre-existing condition like minor back pain, it’s important to understand your health insurance—from enrollment and therapy coverage to prior authorization requirements and appealing denied claims.

Choosing the Right Plan for Chronic Condition Management

To choose the right plan, expats with ongoing back pain should evaluate outpatient benefits, therapy coverage, and cost-sharing details. Since not all policies treat musculoskeletal conditions equally, here is a checklist of what to look for when reviewing your options:

- Coverage of pre-existing conditions: Check if back pain is covered, or if exclusions, waiting periods, or premium loadings apply.

- Physiotherapy and alternative therapy coverage: Confirm whether physiotherapy, chiropractic, or osteopathy sessions are included, and how many visits are allowed per year.

- Prescription drug benefits: Ensure medications for pain management, muscle relaxation, or inflammation are covered under the outpatient drug benefit.

- Specialist access: Look for easy access to orthopedists, rheumatologists, or rehabilitation specialists without excessive referral barriers.

- Out-of-pocket costs: Review deductibles, copayments, and session caps for therapies, prescriptions, and diagnostic imaging.

- Global coverage: Verify that your plan extends to care both in your host country and abroad, especially if you travel frequently.

Importance of Accurate Disclosure During Enrollment

It’s crucial to honestly disclose any pre-existing conditions, including minor back pain, when enrolling in an expat health plan. This transparency helps insurers assess your risk accurately and prevents issues such as rejected claims or policy cancellation.

Being upfront also allows insurers to approve ongoing therapy in advance, providing peace of mind and smoother access to care.

Understanding Your Plan’s Formulary for Back Pain Medications and Supplies

A plan formulary is a tiered list of covered medications and supplies, along with the level of cost-sharing. For minor back pain, typical medications may include NSAIDs, muscle relaxants, or prescribed topical therapies.

Common medications are generally categorized as

- Tier 1: Preferred generic drugs

- Tier 2: Generic drugs

- Tier 3: Preferred brand drugs

- Tier 4: Non-preferred brand drugs

- Tier 5: Specialty tier drugs

Prior Authorization Strategies for Denied Claims

Some treatments or supplies related to back pain may require insurer approval or prior authorization before coverage applies. Examples include:

- Extended courses of physiotherapy or chiropractic care

- Specialized injections or procedures

- Durable medical equipment (e.g., braces, TENS units)

- High-cost medications not on the preferred formulary

In-network providers often handle prior authorization for you, but for out-of-network care, you may need to submit documentation yourself. The process typically takes several business days, so plan ahead to avoid treatment delays.

Handling Denied Claims for Back Pain Care

If your insurer denies a claim for back pain treatment, don’t panic; appeals are possible.

First, review your Explanation of Benefits (EOB) or denial letter to understand the reason. Common denial reasons include exceeding visit limits, lack of prior authorization, non-covered services, or insufficient medical necessity documentation.

Strategies for appealing denied claims include:

- Identify the reason for denial: Clarify whether it relates to policy limits, coding errors, or benefit exclusions.

- Craft a strong appeal letter: Directly address the insurer’s rationale and explain why the treatment is medically necessary.

- Provide supporting documents: Include physician notes, treatment guidelines, and records of prior conservative measures.

- Stay persistent: Keep copies of all correspondence, track follow-ups, and resubmit if needed. Many appeals succeed with persistence.

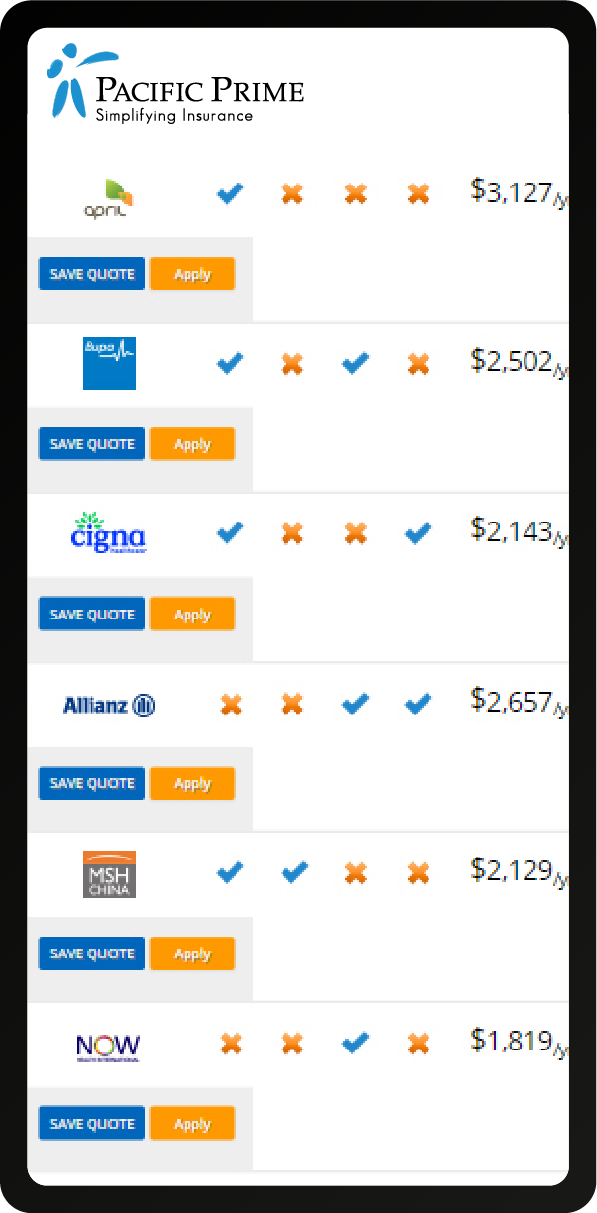

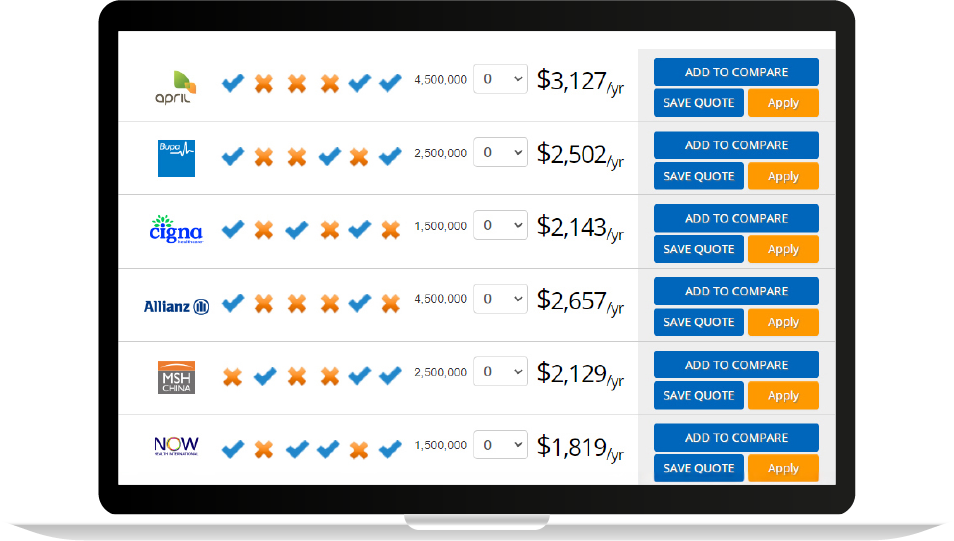

Best International Health Insurance Providers for Expats with Minor Back Pain

Providers like Bupa Global, Allianz, Cigna Global, and GeoBlue offer some of the strongest international health insurance options for expats dealing with minor back pain. These insurers are known for comprehensive outpatient coverage and strong support for managing musculoskeletal conditions abroad.

Bupa Global for Expats with Minor Back Pain

Bupa Global is widely recognized as a premium international health insurer, offering four flexible plan levels: Select, Premier, Elite, and Major Medical, each designed to fit different health needs and budgets.

- Select: ~USD $1,587,100, covering essential inpatient and outpatient care, including day-to-day medical visits.

- Premier: ~USD $2,380,600, with broader benefits including check-ups, dental treatment, and enhanced outpatient coverage.

- Elite: ~USD $4,761,300, featuring family-focused benefits such as maternity and fertility after waiting periods.

- Major Medical: ~USD $3,174,200, focusing on emergencies and major medical costs rather than routine or wellness care.

Bupa Global may provide coverage for pre-existing conditions such as minor back pain, depending on medical underwriting. Disclosure during enrollment is essential, as acceptance often depends on insurer review.

Allianz for Expats with Minor Back Pain

Allianz Care offers modular international health insurance, allowing expats to tailor coverage through three primary tiers: Care, Care Plus, and Care Pro.

- Care: USD $2,500,000, covering inpatient essentials and expat-specific benefits.

- Care Plus: USD $4,000,000, extending to emergency outpatient care and dental.

- Care Pro: USD $5,000,000, adding benefits such as preventive surgery and accidental death coverage.

For expats with back pain, Allianz’s outpatient rider can be especially useful, covering specialist consultations, physiotherapy sessions, prescription drugs, and diagnostic imaging, which are critical components of musculoskeletal care.

Cigna Global for Expats with Minor Back Pain

Cigna Global provides highly customizable health plans with three tiers of coverage: Silver, Gold, and Platinum.

- Silver: USD $1,000,000, covering core inpatient and day-patient needs.

- Gold: USD $2,000,000, expanding coverage for specialist consultations and rehabilitation.

- Platinum: Unlimited annual coverage, with most inpatient and outpatient services covered in full.

Cigna includes a Chronic Condition Program across all tiers, offering personalized support for ongoing health issues like back pain. Add-ons are also available, including outpatient care (key for physiotherapy and pain management prescriptions), wellness programs, and medical evacuation coverage.

GeoBlue for Expats with Minor Back Pain

GeoBlue is a strong choice for American expats abroad, offering two flexible options under its Xplorer series:

- Xplorer Premier: Worldwide coverage, including the U.S., with 80% in-network coinsurance. This option allows policyholders to seek treatment in the U.S. specifically if needed.

- Xplorer Essential: Covers care outside the U.S. only, with optional short-term U.S. emergency coverage.

GeoBlue’s benefits include inpatient and outpatient care, diagnostic testing, surgery, prescription drugs, and mental health services. Importantly, expats with minor back pain may be eligible for immediate coverage of pre-existing conditions if they can provide proof of continuous prior insurance.

6 Tips for Choosing Expat Insurance with Minor Back Pain

Selecting the right international health insurance can be especially important if you have a history of minor back pain. While many expat plans offer coverage for physiotherapy, chiropractic care, or medications, the specifics vary widely between insurers.

To make sure you’re fully protected and avoid costly surprises, keep these six tips in mind:

1. Be Honest and Transparent

When applying for coverage, full disclosure about your back pain history is essential. Even if your condition is mild or intermittent, omitting it could lead to denied claims or policy cancellation later. Transparency ensures your insurer can assess your case properly.

2. Compare Underwriting Philosophies

Not all insurers treat pre-existing conditions the same way. Some impose strict exclusions, while others may offer coverage after a waiting period or with additional premium loading. When comparing plans, prioritize insurers with more flexible approaches to musculoskeletal conditions.

3. Review Policy Wordings Carefully

Always read the fine print. Pay close attention to sections on:

- Pre-existing conditions and how they are defined

- Exclusions that could limit access to physiotherapy or chiropractic sessions

- Waiting periods before certain benefits are available

- Formularies, which determine which pain medications or supportive devices are covered

Understanding these details upfront helps avoid surprises when you need care.

4. Check Network and Direct Billing

Having access to a strong medical network with direct billing can save you time and hassle. This is especially valuable if you need multiple physiotherapy or specialist visits. With direct billing, the provider handles payment directly with the insurer, reducing your upfront costs.

5. Consider Emergency Evacuation

Minor back pain is rarely life-threatening, but complications may require higher-level care unavailable in rural areas. An international plan with emergency evacuation and repatriation ensures quick transfer to a facility equipped to handle serious issues.

6. Seek Expert Advice

Finding an international health insurance plan that covers pre-existing conditions like back pain can be a headache. Consulting an experienced health insurance broker like Pacific Prime can help you compare plans from multiple insurers and select a policy that fits your budget and benefits needs.

Ensure Peace of Mind Abroad with Pacific Prime

Living overseas with minor back pain or any pre-existing condition means choosing your international health insurance carefully. Coverage, premiums, and access to care can all be affected if your condition isn’t properly considered.

With over 25 years of experience, Pacific Prime guides expats through the complex insurance landscape, helping you find a plan tailored to your needs, whether it’s comprehensive international coverage, family plans, or short-term policies.

Get in touch today for a FREE quote comparison and impartial expert advice, and travel or live abroad with confidence knowing your healthcare is covered.

Frequently Asked Questions

Is minor back pain covered under insurance?

Coverage for minor back pain depends on the insurer, plan level, and medical underwriting. Some plans may include physiotherapy, chiropractic care, or pain medication under outpatient benefits, while others could impose waiting periods, exclusions, or benefit limits for pre-existing conditions.

Does minor back pain require a medical diagnosis?

A formal diagnosis through physical examination, imaging (such as X-ray or MRI), or specialist evaluation is important both for creating an effective treatment plan and for securing insurance coverage. Without documentation, insurers may deny claims related to back pain.

Can you travel with minor back pain?

Expats with back pain can travel safely by planning ahead, packing necessary medications, using supportive devices (like braces), staying mobile during long flights, and ensuring their international health insurance covers outpatient treatments or emergencies abroad.

How do I compare plans for back pain coverage abroad?

When reviewing options, look closely at how each plan handles pre-existing conditions, physiotherapy session limits, outpatient drug formularies, access to specialists, and whether global coverage applies while traveling. Consulting a broker or using a comparison tool can make this process easier.

What happens if a back pain claim is denied?

Claims may be denied for reasons like non-disclosure of a pre-existing condition, missing prior authorization, or benefit limits being exceeded. You can appeal by providing medical records, a doctor’s statement of medical necessity, or supporting clinical evidence to strengthen your case.

With his keen interest in journalism, especially in the healthcare and wellness field, Tawan joins Pacific Prime with the goal of creating content that simplifies health insurance solutions, helping people make informed choices and choose the best options for their needs. Tawan firmly believes that words have power that can shape the world for the better.

In his free time, Tawan loves to pick up his Nintendo Switch and wield his Master Sword in Hyrule’s dungeons. He is also an avid sci-fi books/shows enjoyer. You can spot him hanging around bookstores and game shops all day long!

- Best Health Insurance for Solo Traveling in Thailand – October 22, 2025

- Top Health Insurance in Thailand for Irish Expats: Options and Benefits – October 18, 2025

- Daman Health Insurance for Expats in Dubai: Plans, Benefits, and Options – October 15, 2025