300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Living abroad with asthma can raise important questions: Will your medication be covered overseas? What happens if you need emergency care during a flare-up? Can you find a plan that supports long-term respiratory health?

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

For expats, understanding how asthma affects health insurance is key to staying protected. This guide breaks down what to expect and how to choose a plan that supports long-term respiratory health.

Note: If you have asthma before joining a health insurance plan, your coverage may be subject to medical underwriting. Insurers will assess your current health condition—including severity, control, and recent treatment history—before confirming coverage.

Understanding Asthma

Asthma is a chronic respiratory condition that causes inflammation and narrowing of the airways, making it difficult to breathe. It can range from mild to severe, and is typically classified into types such as allergic asthma, exercise-induced asthma, and occupational asthma.

Common symptoms include wheezing, coughing, chest tightness, and shortness of breath. Triggers vary by individual but often include allergens, pollution, cold air, stress, and respiratory infections.

Asthma can significantly impact daily life, especially if it is poorly managed. Severe attacks may require emergency care or hospitalization, making consistent treatment and monitoring essential.

Diagnosis typically involves lung function tests like spirometry, and long-term management focuses on controlling symptoms, preventing flare-ups, and maintaining quality of life through medication and lifestyle adjustments.

How Asthma Affects Health Insurance

Asthma affects health insurance by requiring coverage for ongoing care and medications. Comprehensive plans with low deductibles are often the best for moderate to severe cases. Even with insurance, costs can add up–making coverage essential to avoid ER visits and hospitalizations.

Pre-existing Condition Status

Asthma is considered a pre-existing condition by most insurers. This means your health history, including severity, control, and recent treatments, may be reviewed before coverage is approved. In some cases, this process is called medical underwriting.

Under ACA-compliant plans (such as those in the U.S. under the Affordable Care Act), insurers cannot deny coverage or charge higher premiums based solely on asthma. These plans also prohibit waiting periods for pre-existing conditions.

However, non-ACA plans, short-term policies, or international insurers may still apply waiting periods, exclusions, or premium adjustments based on your current health status. Always check whether your plan follows ACA-style protections or requires underwriting.

Impact on Health Insurance Premiums

Premiums aren’t always directly increased due to asthma, especially under ACA-compliant plans. However, factors like severity, frequency of attacks, and co-existing conditions (e.g., allergies or obesity) can influence pricing in certain markets. Well-controlled asthma often helps maintain stable rates.

Coverage for Asthma Management

Managing asthma effectively requires consistent access to care, medication, and monitoring tools. Health insurance plays a vital role in covering these essentials, especially for expats navigating unfamiliar healthcare systems.

Most comprehensive plans include coverage for:

- Routine visits to primary care physicians, pulmonologists, and allergists

- Medications, including:

- Controller drugs (inhaled corticosteroids, long-acting bronchodilators)

- Rescue inhalers (short-acting bronchodilators)

- Biologic therapies for severe asthma

- Coverage tiers and formularies vary by plan

- Devices and supplies, such as:

- Inhalers, nebulizers, spacers, peak flow meters

- Diagnostic tests, including spirometry, allergy testing, and imaging

- Emergency care, including urgent care visits, ER treatment, and hospital stays for severe attacks

Navigating Health Insurance with Asthma

Managing asthma abroad requires more than just access to medication; it demands a health insurance plan that supports long-term respiratory care.

From routine checkups to emergency treatment, understanding how your policy addresses chronic conditions is crucial to maintaining your health and avoiding unexpected expenses.

Choosing the Right Plan That Supports Asthma Management

Not all health insurance plans are designed with chronic respiratory conditions in mind. For expats managing asthma, it’s essential to choose a plan that goes beyond basic emergency coverage and supports long-term disease management.

Plans with low deductibles, broad specialist access, and robust outpatient benefits tend to be more cost-effective and better suited for individuals with moderate to severe asthma.

Look for coverage that includes:

- Outpatient visits to pulmonologists, allergists, and primary care physicians for regular checkups and symptom monitoring

- Prescription drug benefits for both controller medications (e.g., inhaled corticosteroids, long-acting bronchodilators) and rescue inhalers (e.g., short-acting bronchodilators)

- Emergency care for asthma attacks, including urgent care visits, ER treatment, and hospital stays

- Diagnostic testing, such as spirometry, allergy screening, and imaging, is used to assess lung function and identify triggers

- Medical devices and supplies like inhalers, nebulizers, spacers, and peak flow meters to support daily management

Disclosing Your Asthma Diagnosis During Enrollment

Accurate disclosure is essential when applying for health insurance. Asthma is considered a pre-existing condition, and insurers may evaluate your current health status before approving coverage. Failure to disclose can lead to denied claims or policy cancellation.

Key details to disclose:

- Diagnosis date and severity

- Medications and devices used

- Frequency of flare-ups or hospital visits

- Any related conditions (e.g., allergies, COPD)

Reviewing Your Plan’s Formulary for Asthma Medications and Devices

A formulary outlines which medications and devices your insurer covers, and at what costs. Asthma drugs may be split into tiers, affecting copays. Check if your current prescriptions, inhalers, and biologics are included to avoid unexpected pharmacy expenses.

Some plans may only cover generics or require switching brands. Devices like nebulizers or spacers might need a prescription or fall under durable medical equipment. Reviewing the formulary before enrolling helps ensure your asthma care is uninterrupted.

Navigating Prior Authorization for High-Cost Asthma Treatments

Biologic therapies for severe asthma, like Xolair or Dupixent, often require prior authorization. This means your doctor must prove medical necessity before the insurer approves coverage. The process can take time, so starting early is key.

Ask your provider to submit documentation promptly and follow up with your insurer to track progress. Keep records of all communication. Delays in approval can disrupt treatment, so staying proactive helps avoid gaps in care.

Appealing Denied Claims for Asthma Care

If your insurer denies coverage for asthma-related treatment, you have the right to appeal. Many denials are reversed when supported by strong medical evidence and clear documentation from your healthcare provider.

Start by reviewing the denial letter and your policy details. Gather medical records, a physician’s statement, and any relevant test results. Submit a formal appeal and follow up regularly. Persistence and clarity often lead to a successful outcome.

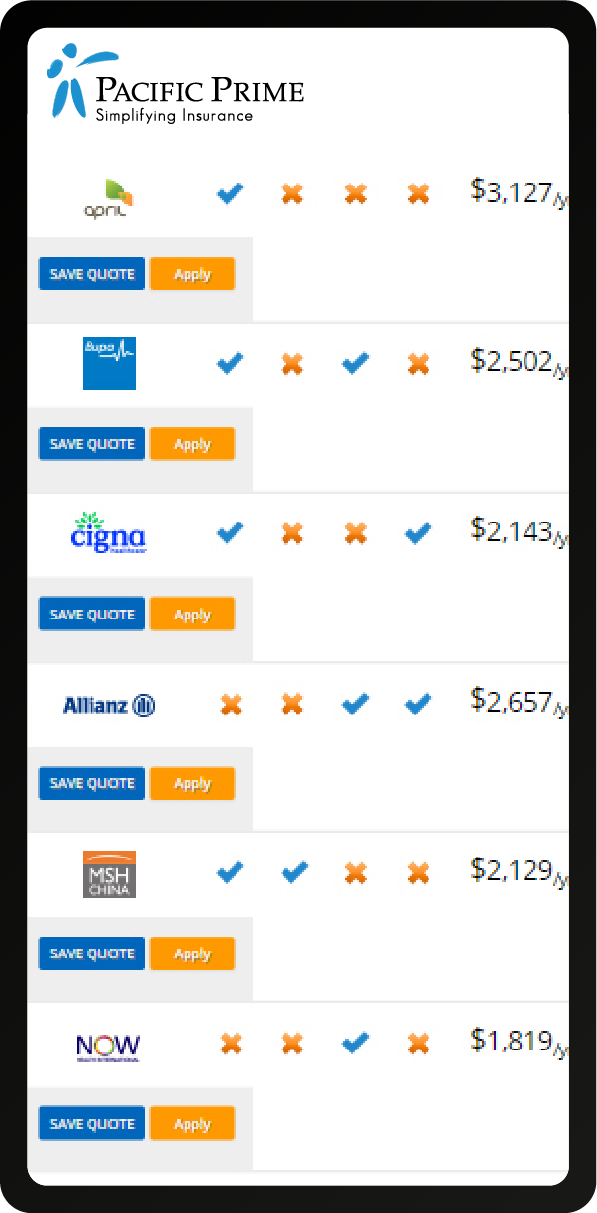

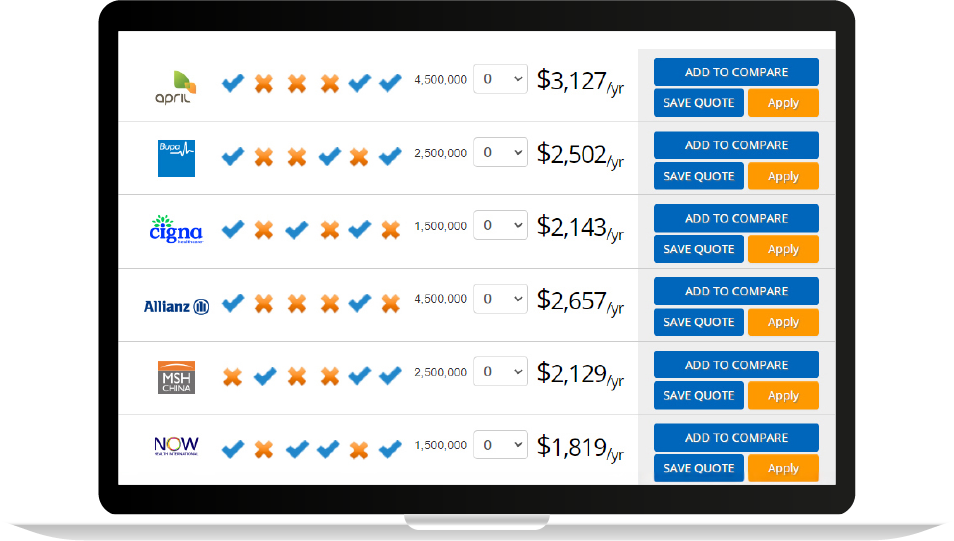

Best Health Insurance Providers for Expats with Asthma

Managing asthma abroad means finding a health insurance plan that supports long-term care, access to specialists, and essential medications. The best providers offer flexible coverage—even for pre-existing conditions—making it easier to stay healthy while living overseas.

Cigna Global

Cigna Global is known for its customizable international health insurance plans and strong support for chronic conditions. Their modular structure allows expats to tailor coverage to their medical needs and lifestyle.

Cigna Plan Tiers:

- Silver: Covers inpatient services and emergency medical care

- Gold: Adds outpatient visits, prescription benefits, and preventive screenings

- Platinum: Includes dental and vision, direct access to specialists, wellness programs, and mental health support

IMG Global Medical

IMG (International Medical Group) offers a range of international health insurance plans suitable for both short-term and long-term stays. Their coverage includes key benefits for chronic conditions like asthma, with access to prescriptions, diagnostics, and emergency care.

IMG Plan Options:

- Patriot International: Short-term emergency coverage, evacuation, and repatriation

- Global Medical Insurance: Full inpatient and outpatient care, prescriptions, and chronic condition support

- Student Health Advantage: Preventive services, mental health care, and coverage for pre-existing conditions after a waiting period

Bupa Global

Bupa Global provides premium international health insurance with extensive benefits for chronic respiratory conditions. Their plans include access to elite medical facilities and personalized care.

Bupa Plan Highlights:

- Select: Inpatient and outpatient care with basic chronic condition coverage

- Premier: Direct access to specialists, prescription benefits, and preventive screenings

- Elite: Access to top-tier hospitals, second medical opinions, full chronic disease support, plus mental health, dental, vision, and wellness services

William Russell

Willim Russell offers flexible international plans with transparent underwriting. They’re a strong choice for expats with well-managed asthma seeking personalized coverage.

William Russell Plan Levels:

- Bronze: Inpatient-only coverage and emergency services

- Silver: Outpatient consultations, diagnostics, and prescription coverage

- Gold: Mental health services, lifestyle support, and chronic condition monitoring

- Platinum: Worldwide coverage, direct billing, and enhanced wellness benefits

GeoBlue International

Designed specifically for U.S. citizens living overseas, GeoBlue’s Xplorer plans offer seamless coordination with the Blue Cross Blue Shield network for care back in the States. It’s a top pick for those focused on preventive services and long-term management of chronic conditions such as asthma.

GeoBlue Xplorer Options:

- Essential: Emergency medical care abroad, hospitalization, and evacuation

- Premier: Comprehensive outpatient coverage, chronic condition support, prescriptions, and access to the U.S. PPO network

Planning for Asthma Care Abroad

Asthma is a manageable condition–but only when you have consistent access to the care and medications you need. Choosing the right health insurance plan is a key part of that equation, especially when living overseas. And Pacific Prime is here to help you find that perfect plan.

Pacific Prime works with leading insurers to help expats find coverage that fits their respiratory health needs, lifestyle, and location. Our team offers personalized support, from comparing quotes to navigating underwriting, so you can make confident, informed decisions about your health insurance.

Contact us today and get a free quote comparison!

Frequently Asked Questions

Will health insurance cover asthma medications abroad?

Coverage for asthma medications depends on your plan’s formulary. Most comprehensive policies include common prescriptions like inhalers and corticosteroids, but coverage levels and out-of-pocket costs can vary based on drug tiers and regional availability.

Do I need to disclose my asthma diagnosis when applying for insurance?

Disclosing your asthma diagnosis during enrollment is essential. Insurers assess your current health condition to determine coverage eligibility, and withholding information can lead to denied claims or policy cancellation later on.

Are advanced asthma treatments typically covered by insurance?

Coverage for advanced treatments often depends on your plan’s benefits and approval process. Some therapies may require prior authorization, meaning your doctor must show medical necessity before coverage is granted. Reviewing your policy details is essential.

How does asthma influence health insurance premiums?

Premiums are influenced by several factors, including the severity and control of your asthma, your overall health, and the insurer’s underwriting guidelines. Well-managed asthma may result in more favorable terms, while frequent complications could affect pricing.

What steps should I take if my asthma-related claim is denied?

Review the denial notice and your policy. Gather medical records and a doctor’s letter, then submit a formal appeal. Strong documentation can help, but outcomes vary based on the insurer and case specifics. Staying organized and persistent improves your chances.

At Pacific Prime, Grace focuses on simplifying complex concepts on international health insurance to make these topics easily accessible and understandable for our target audience. Being a Filipino born in Hong Kong, she understands the struggles of most immigrants and expats in finding the right insurance solutions while in another country. Her goal is to redefine most people’s perception of insurance, that it is an investment for one’s protection and future.

In her spare time, Grace is either at home or at Hong Kong Disneyland. She loves reading, watching movies and K-dramas, and attending dance classes.

- How to Find Digital Nomad Jobs in Thailand – October 22, 2025

- Top 12 Insurance Companies in Serbia for Expats – October 21, 2025

- Expat’s Guide: Pros and Cons of Living in Thailand – October 20, 2025