300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Thailand continues to attract expats with its tropical lifestyle, affordable living, and modern infrastructure. But with new tax regulations in 2025, understanding how taxes in Thailand for expats work is essential for staying compliant and financially secure.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

This Pacific Prime article breaks down everything you need to know about Thailand’s 2025 tax rules, from residency status and income categories to deductions, remittance strategies, and compliance tips.

Whether you’re new to Thailand or a seasoned expat, this resource will help you navigate the tax landscape with clarity and confidence.

Understanding Thailand’s Tax System

Thailand’s personal income tax (PIT) is progressive, ranging from 5% to 35%. The tax year runs from January 1 to December 31, and expats must file annual returns with the Thai Revenue Department (either online or in person) by March 31 of the following year.

Tax Rates and Brackets

Thailand’s PIT rates range from 5% to 35%, with exemptions for low-income earners. These brackets apply to both residents and non-residents, depending on the nature and source of income.

The rates below apply to net taxable income after deductions and allowances are applied. Understanding your bracket is key to estimating your annual tax liability.

| Annual Income (THB) | Tax Rate |

| 0 – 150,000 | Exempt |

| 150,001 – 300,000 | 5% |

| 300,001 – 500,000 | 10% |

| 500,001 – 750,000 | 15% |

| 750,001 – 1,000,000 | 20% |

| 1,000,001 – 2,000,000 | 25% |

| 2,000,001 – 5,000,000 | 30% |

| Over 5,000,000 | 35% |

Filing Methods and Deadlines

Filing can be done online via the Thai Revenue Department’s e-filing portal or in person at local offices. Payment options include bank transfer, credit card, or cash at designated banks. Late filings may incur penalties, so mark your calendar early.

Expats must file taxes using one of two forms:

- PND 90: For multiple income sources (freelance, rental, investments)

- PND 91: For employment income only

Tax Residency and Its Impact

Residency status plays a central role in determining how taxes in Thailand for expats are calculated. You’re considered a tax resident if you spend 180 days or more in Thailand during a calendar year.

Tax residents are subject to Thai tax on both local income and foreign income remitted into Thailand. Non-residents, on the other hand, are taxed only on income earned within Thailand. This distinction affects how you report and remit funds.

Taxable Income Categories

Thailand taxes a wide range of income types. If you’re an expat earning or remitting income into Thailand, it may be subject to tax. Even income earned abroad may be taxed if it’s transferred into Thailand.

Common taxable income:

- Salaries and wages

- Freelance and business income

- Rental income from Thai properties

- Capital gains and investment returns

- Pensions and retirement income

- Cryptocurrency and digital assets

Foreign Income Remittance Rules (2025 Update)

A major clarification in 2025 affects how foreign income is taxed. The Thai Revenue Department confirmed that only foreign income earned from January 1, 2024, onward is taxable if remitted into Thailand.

This means:

- Income earned before 2024 is not taxable, even if transferred into Thailand in 2025 or later.

- Income earned in 2024 or later is taxable in the year it is remitted.

This clarification provides relief for retirees and long-term expats who had previously earned income abroad and were concerned about retroactive taxation.

Strategic Remittance Planning

Remittance planning is especially important for those with passive income, pensions, or investment earnings abroad. To manage taxes in Thailand for expats, plan foreign transfers carefully:

- Avoid remitting large lump sums without tax planning

- Keep records of income origin and transfer dates

- Consult a tax advisor for cross-border strategies

- Consider timing transfers across tax years to reduce liability

Tax Deductions and Allowances in Thailand

In Thailand, tax deductions and personal allowances help reduce your taxable income. These include standard expense deductions, family-related allowances, and specific itemized deductions like insurance premiums and charitable donations.

Deductions and allowances apply only to tax residents (180+days in Thailand). You must provide receipts and documentation to claim itemized deductions. Some deductions, like Retirement Mutual Funds (RMFs) and insurance, require Thai-registered providers.

Expense-Based Deductions

Expense-based deductions apply to income from employment, services, and rental activities. These are calculated as a fixed percentage of gross income, with caps depending on the category. They help simplify reporting and reduce taxable income without itemizing every expense.

- Employment income: 50% of income, capped at THB100,000

- Service fees, commissions, director fees: 50% of income, capped at THB100,000

- Rental Income:

- 30% of buildings and vehicles

- 20% for agricultural land

- 15% for other property types

Itemized Deductions

Itemized deductions allow taxpayers to subtract specific expenses from their income. These include contributions to retirement funds, insurance premiums, and charitable donations. Proper documentation is required. And some deductions have percentage or monetary caps.

- Life insurance premiums: Up to THB100,000

- Health insurance premiums: Up to THB25,000

- Social security contributions: Fully deductible

- Retirement Mutual Funds (RMFs): Up to 30% of income, capped at THB500,000

- Super Savings Funds (SSFs): Up to THB200,000

- National Pension Fund contributions: Deductible within limits

- Charitable donations: Up to 10% of net income after other deductions

- Mortgage interest (first home): Up to THB100,000

Personal Allowances

Personal allowances are fixed amounts that reduce taxable income based on family and personal circumstances. These include supporting a spouse, children, elderly parents, and dependents with disabilities. They are claimed annually and require basic documentation.

- Personal allowance: THB60,000

- Spouse (non-income earning): THB60,000

- Children: THB30,000 per child (up to 3 children)

- Parental support: THB30,000 per supported parent (age 60+)

- Pregnancy and childbirth expenses: Up to THB60,000

- Child education expenses: THB30,000 per child

- Disabled dependent: THB60,000 per person

Double Taxation Agreements (DTAs)

Thailand has DTAs with many countries to prevent double taxation. These agreements allow expats to offset foreign taxes paid against Thai liabilities.

To claim treaty benefits, you’ll need proof of foreign tax paid, a Thai tax residency certificate, and supporting income documentation. DTAs are especially helpful got expats with income from multiple jurisdictions.

Countries with DTAs include:

- United States

- United Kingdom

- australia

- Canada

- Germany

- France

- Japan

Compliance and Planning Tips

Planning ahead can help you avoid penalties and reduce your tax liability. Many expats benefit from working with bilingual accountants or firms that specialize in cross-border taxation. To stay compliant with taxes in Thailand for expats, follow these best practices:

- Track your days in Thailand to confirm residency

- Maintain records of income sources and remittance dates

- Use checklists and reminders for filing deadlines

- Work with a tax advisor familiar with Thai and international law.

Avoiding Common Mistakes

Mistakes can lead to audits, fines, or delayed refunds. Staying organized and informed is your best defense. Here are some common mistakes you should avoid when doing your taxes in Thailand.

- Missing the March 31 deadline

- Failing to declare foreign income remitted

- Incorrect residency status

- Incomplete documentation for deductions

- Overlooking DTA benefits

How Health Insurance Can Help Lower Your Taxes

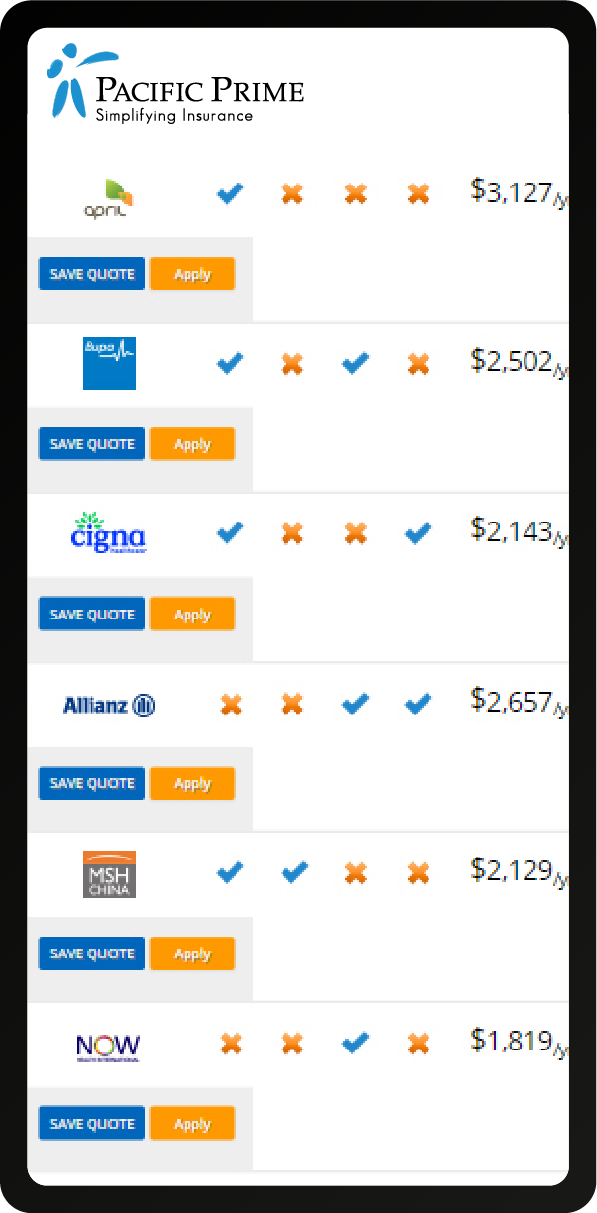

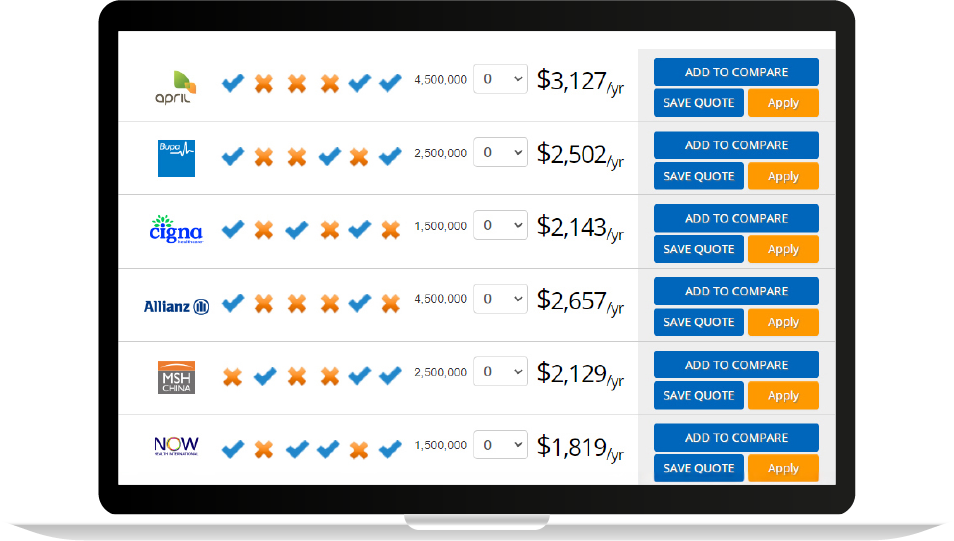

For expats living in Thailand, health insurance offers more than peace of mind; it can also reduce your tax bill. Under Thai tax law, tax residents may deduct up to THB25,000 per year in health insurance premiums, provided the policy meets specific criteria.

Eligibility for Tax Deduction

Not all health insurance plans are eligible for tax deduction, especially those issued by foreign providers. Thailand’s Revenue Department requires that the policy be issued by a Thai-registered insurance company or distributed through a licensed Thai broker.

This ensures the policy complies with local standards and reporting requirements. International health insurance may qualify only if it’s underwritten by a Thai insurer or distributed through a Thai-licensed broker.

To qualify for the THB25,000 health insurance deduction:

- The policy must be issued by a Thai-registered insurance company

- It must be a personal policy, not corporate or employer-sponsored

- You must be a tax resident (180+ days in Thailand)

- You must retain receipts or proof of premium payments

Tax-Smart Living in Thailand with Pacific Prime

Living in Thailand as an expat comes with lifestyle perks, but also financial responsibilities. Understanding how to navigate taxes, deductions, and residency rules is key to long-term success and peace of mind.

Pacific Prime offers tailored health insurance plans that meet Thai tax deduction rules. Our expert team helps expats protect their well-being and legally lower taxable income, making us a valuable partner in your financial journey abroad.

Need help choosing a compliant health insurance plan or optimizing your tax strategy? Contact us and get a quote today!.

Frequently Asked Questions

Do I need to pay Thai taxes if I only earn income from abroad?

If you are a tax resident in Thailand (i.e., you stay 180 days or more in a calendar year), you are required to pay tax on foreign income, but only if it is earned in 2024 or later and remitted into Thailand. Income earned before 2024 is exempt, even if transferred now.

What counts as taxable income for expats in Thailand?

Taxable income includes employment income, freelance earnings, rental income, capital gains, pensions, dividends, and even cryptocurrency profits. If you’re a tax resident and remit qualifying income into Thailand, it may be subject to tax.

Can I reduce my taxes with deductions and allowances?

Thailand offers a range of deductions and allowances for tax residents. These include expense-based deductions, contributions to retirement funds, charitable donations, and health insurance premiums.

Is health insurance tax-deductible for expats?

Health insurance premiums are tax-deductible up to THB25,000 per year, but only if the policy is issued by a Thai-registered insurer. International plans may qualify if underwritten or distributed by a licensed Thai provider.

What happens if I miss the tax filing deadline?

The deadline for filing personal income tax in Thailand is March 31 of the following year. Late filings may result in penalties and interest charges. It’s best to file early and keep documentation organized to avoid issues with the Revenue Department.

At Pacific Prime, Grace focuses on simplifying complex concepts on international health insurance to make these topics easily accessible and understandable for our target audience. Being a Filipino born in Hong Kong, she understands the struggles of most immigrants and expats in finding the right insurance solutions while in another country. Her goal is to redefine most people’s perception of insurance, that it is an investment for one’s protection and future.

In her spare time, Grace is either at home or at Hong Kong Disneyland. She loves reading, watching movies and K-dramas, and attending dance classes.

- How to Find Digital Nomad Jobs in Thailand – October 22, 2025

- Top 12 Insurance Companies in Serbia for Expats – October 21, 2025

- Expat’s Guide: Pros and Cons of Living in Thailand – October 20, 2025