300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

It can be tempting to look for the least expensive medical insurance possible as health insurance premiums and healthcare costs continue to rise. The better solution is to maintain sufficient coverage but to secure plans early, utilize deductibles, and compare providers to save money.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Are you looking for ways to lower your health insurance premiums? Are you unsure how to get less expensive care without compromising on important medical coverage?

In this Pacific Prime article, our specialists will walk you through seven practical tips on lowering health insurance premiums and explain the importance of health insurance.

Seven Tips On Reducing Your Health Insurance Premiums in 2025

You can find the best price for your health insurance plan by getting insured while you’re young, selecting a plan without unnecessary benefits, opting for deductibles, considering inpatient-only plans, asking about discounts, buying a top-up policy, and working with a broker to compare providers.

1. Get Insured While You’re Still Young

Usually, the younger you are, the lower your premium: younger people tend to develop fewer chronic health conditions than the elderly. If you purchase health insurance at an old age, the insurer may view your health conditions as pre-existing conditions, which are often excluded from coverage.

Listed below are the key reasons why younger people pay lower premiums:

- Lower Risk Profile: Younger people are statistically less likely to develop chronic illnesses or require frequent medical care, making them less risky to insure.

- Healthier Lifestyle: Younger individuals often have healthier habits (e.g., regular exercise, balanced diet), reducing the likelihood of claims.

- Fewer Pre-Existing Conditions: Younger adults typically have fewer diagnosed health issues, which insurers consider when calculating premiums.

Listed below are the advantages of buying insurance early on in your life:

- Lock in Lower Premiums: Premiums are based on your age at the time of purchase. Buying early allows you to secure lower rates that remain stable (or increase minimally) over time.

- Avoid Coverage Exclusions: If you wait until an older age to buy insurance, any health issues you develop (e.g., diabetes, hypertension) may be classified as pre-existing conditions and be excluded from coverage.

- Build a Longer Coverage History: Starting early helps you establish a longer relationship with the insurer, which can be beneficial for future policy renewals or upgrades.

- Access to Comprehensive Plans: Younger individuals are more likely to qualify for plans with broader coverage and fewer restrictions.

2. Select a Plan with the Right Benefit Limits

Benefit limits are the maximum amounts the insurer will pay out for each benefit. You should consult an insurance expert to assess your health insurance needs and opt for the right sum assured according to your age and health status.

These limits can apply to:

- Overall coverage: This is the total sum insured per year.

- Specific categories: This applies to different coverage types such as hospitalization, surgery, outpatient care, or prescription drugs.

- Lifetime limits: This refers to the maximum payout over the policy’s duration.

Listed below are some reasons why the right benefits matter:

- Avoid Underinsurance: Low benefit limits may leave you paying out of pocket for expensive treatments.

- Prevent Overinsurance: Excessively high limits can lead to unnecessarily high premiums.

- Tailored Coverage: Aligning limits with your needs ensures you’re protected where it matters most.

3. Opt for Deductibles

Deductibles are the amount you pay out of pocket before the insurer will start paying for medical services. While deductibles can lower health insurance premiums, you should consult insurance professionals to find the right amount of deductible.

For example, if your plan has a $1,000 deductible, you pay the first $1,000 of medical expenses each year, and the insurer covers the rest (subject to policy terms).

4. Consider Getting an Inpatient-Only Plan

An inpatient-only plan is a basic health insurance option that covers medical expenses only when you are hospitalized. While it offers limited coverage compared to comprehensive plans, it can be a cost-effective solution for certain individuals.

Here’s a detailed breakdown:

- Definition: An inpatient health insurance plan covers expenses related to hospitalization, such as room charges, surgeries, and intensive care, but excludes outpatient care, such as doctor visits, diagnostic tests, prescriptions.

- Scope: Coverage is triggered only when you are formally admitted to a hospital for treatment.

Listed below are those who should consider an inpatient-only plan:

- Young and Healthy Individuals: Those who rarely need medical care and primarily want protection against high hospitalization costs.

- Budget-Conscious Buyers: Individuals who cannot afford comprehensive plans but want basic coverage for emergencies.

- Supplemental Coverage: People who already have limited coverage (e.g., through an employer) and want additional protection for hospitalization.

- Low-Risk Individuals: Those with no chronic conditions or frequent medical needs.

5. Ask About Family Discounts

Family discounts are a valuable feature offered by many health insurance providers, allowing you to cover multiple family members under a single policy at a reduced cost compared to individual plans.

Here’s a detailed breakdown of family discounts:

- Definition: A pricing incentive offered by insurers to encourage families to enroll under a single policy.

- Coverage: Typically includes the primary policyholder, spouse, and dependent children (sometimes extended to parents or in-laws).

- Cost Savings: Premiums for a family plan are usually lower than the combined cost of individual plans for each member.

6. Buy a Top-Up Plan

A top-up plan is an additional health insurance policy designed to complement your existing coverage by providing extra financial protection for high medical expenses. It acts as a cost-effective way to enhance your coverage without purchasing a completely new policy.

Here’s a detailed breakdown:

- Definition: A top-up plan is a supplementary health insurance plan that kicks in after you exceed a specified threshold (called the deductible) on your primary policy.

- Purpose: Top-up plans cover high medical costs that exceed the limits of your base insurance plan.

- Example: If your primary plan covers up to $5,000 and you opt for a top-up plan with a $3,000 deductible, the top-up plan will cover expenses beyond $8,000 ($5,000 + $3,000).

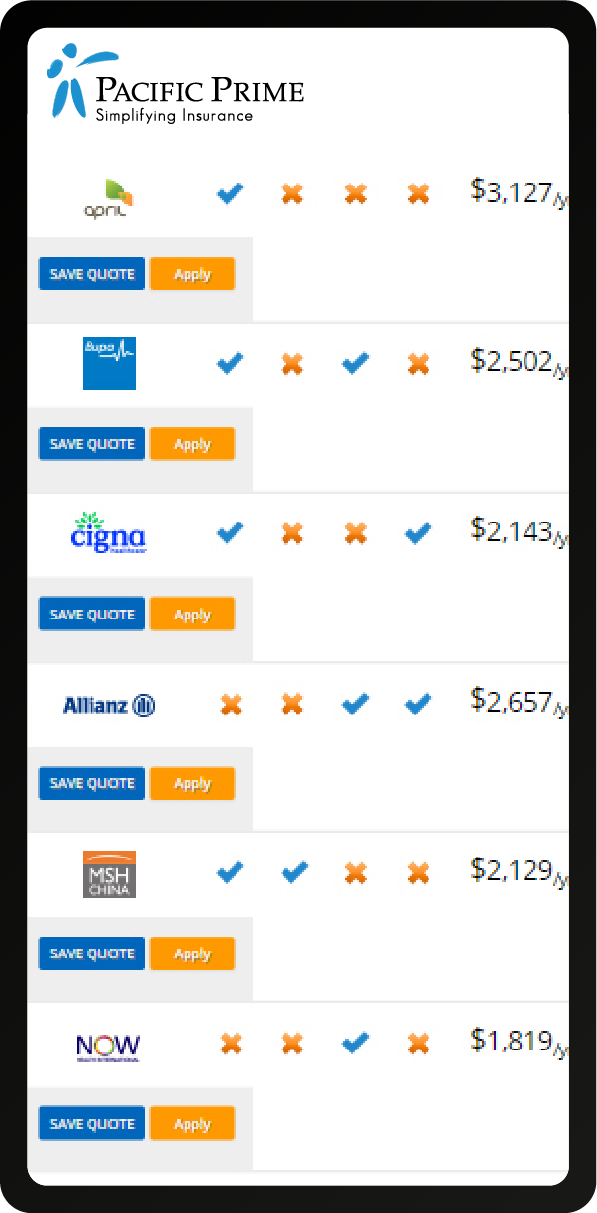

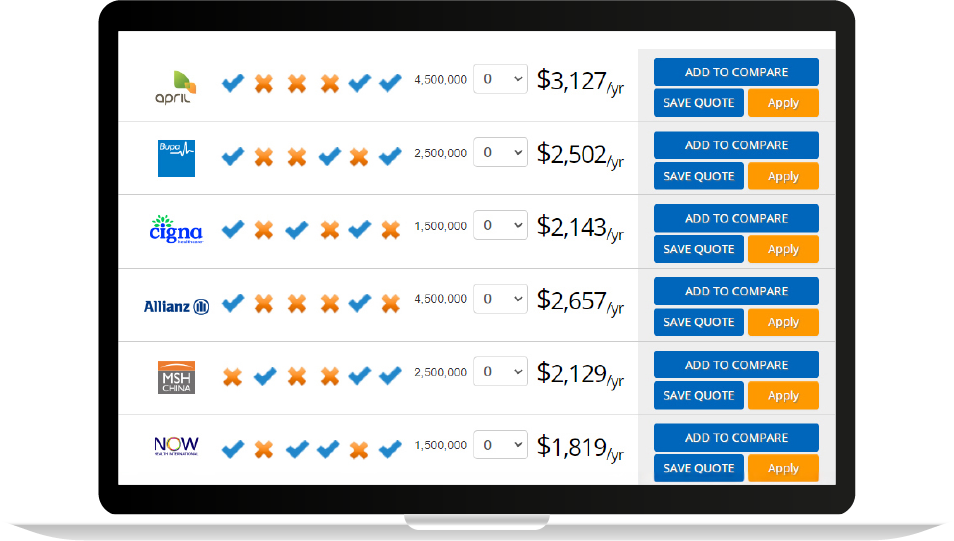

7. Compare Health Insurance Plans

It is cost effective to consult an insurance broker for plan comparisons. While lower insurance premiums may seem desirable, let’s not forget the original purpose of securing health insurance is to obtain financial protection.

Consulting an insurance broker or professional can help you navigate the complexities of different plans and choose one that matches your budget and healthcare needs. When comparing health insurance plans, consider the following key factors:

- Coverage Needs: Assess your and your family’s specific healthcare requirements, including regular medications, planned procedures, and preferred healthcare providers.

- Plan Types: Understand the differences between plan types such as HMO, PPO, EPO, and POS, which affect your choice of healthcare providers and referral requirements.

- Costs: Evaluate all associated costs, including premiums, deductibles, copayments, coinsurance, and out-of-pocket maximums, to determine the plan’s affordability.

- Provider Networks: Ensure your preferred doctors, specialists, and hospitals are within the plan’s network to avoid higher out-of-pocket expenses.

- Prescription Drug Coverage: Verify that your necessary medications are covered under the plan’s formulary and understand any associated costs.

- Plan Ratings: Review the plan’s quality ratings to assess overall performance and member satisfaction.

- Additional Benefits: Consider any extra services offered, such as wellness programs, telehealth options, or dental and vision coverage, which may add value to the plan.

A Wealth of Insurance Resources at Your Fingertips

If you’d like to learn more about various insurance subjects, visit our blog and video page so that you can understand more about insurance jargon and make an informed decision.

If you want to discuss your health insurance options, whether it’s an international health insurance plan or a local health insurance plan, our team of experts at Pacific Prime is only one phone call or email away.

Contact us to talk to one of our expert advisors or to receive a free, no-obligation quote or plan comparison today!

Frequently Asked Questions

How can I lower my health insurance premiums?

Consider enrolling in a high-deductible health plan paired with a Health Savings Account (HSA). This combination often results in lower premiums and offers tax advantages.

Does maintaining a healthy lifestyle impact my insurance costs?

Adopting healthier habits can reduce healthcare expenses. Some insurers offer discounts for participating in wellness programs, such as gym memberships or smoking cessation initiatives.

Are there specific plan options that can help me save on premiums?

Opting for plans with higher deductibles can lower your monthly premiums. Additionally, choosing policies with co-payment clauses may further reduce premium costs.

Upon graduating from Mahidol University International College’s International Relations program, he spent his career in marketing and business development, working for an international subcontractor, a marketing research firm, an international news agency, a software development company, and a creative agency. His journey now continues at Pacific Prime, where he hopes to make an impact by simplifying insurance and writing a gargantuan amount of SEO articles to draw in billions of leads.

In his free time, Piyanat is an avid martial artist and musician, spending most of his time at boxing gyms in Nakhon Pathom and music studios with his friends in the music industry.

- Chiang Mai Travel Insurance: A Comparison Of The Top Providers – August 22, 2025

- Last-Minute Travel Insurance: How to Get Covered After Departure – August 18, 2025

- Childbirth Coverage in Singapore: Maternity Health Insurance Explained – August 18, 2025