300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Whether you plan to travel extensively overseas, you just turned twenty-six and got bumped from your parent’s health insurance, or you’re in between plans from a job change or other life event, your best temporary options for medical coverage are COBRA, ACA, or short-term health insurance plans.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Are you looking for temporary health insurance for you or a loved one? Even if jargon like ACA or short-term plans is familiar to you, picking the right plan can feel downright intimidating, especially when you throw budget and personal health concerns into the mix.

To help you find the best short-term health insurance for you, this article will outline the different options for temporary health insurance and guide you through what you need to know about each plan, how to qualify, and what you should consider before purchasing your health insurance plan.

Types of Temporary Health Insurance Coverage

For those living outside of the United States who are searching for temporary coverage for medical needs, look for international short-term health insurance.

For those living in the United States, the three main types of health insurance to consider are COBRA plans, ACA plans, and short-term plans—unless you qualify for Medicaid or Medicare. They each have different benefits and setbacks, but they’re each worth considering.

Temporary Health Insurance Coverage in the United States

Short-term health insurance offers flexible, customizable coverage for a few weeks up to a year.

While short-term insurance is available in most states, you can no longer purchase short-term health insurance in Hawaii, Washington, California, Colorado, New Mexico, Minnesota, D.C., New York, New Jersey, Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, or Maine. Similarly, Oregon, Delaware and Maryland restrict short-term-plan coverage to three months or less.

These restrictions apply as an attempt to ensure that individuals receive comprehensive care for the ten essential health benefits (EHBs): ambulatory patient services, hospitalization, mental health and substance use disorder services, emergency services, maternity and newborn care, laboratory services, prescription drugs, pediatric services, rehabilitative services, and preventative wellness and chronic disease care.

If you live in a state which restricts short-term health insurance, look into a COBRA plan or an ACA plan.

COBRA Plans

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is a law in the U.S. that allows you to extend the health insurance coverage you received from your previous employer after you have lost that coverage.

Since your employer no longer covers the cost, you are responsible for payment in full.

The continuity of care available through COBRA plans makes them a tempting option for those with specific health concerns, like chronic illness or regular medical needs, who have established providers and services that suit them.

COBRA plans also tend to be more comprehensive than short-term health insurance, so they’re dependable in both familiarity and scope.

To qualify for COBRA, you must have a distinguishing life event such as voluntary or involuntary job loss, a qualifying move, retirement, reduced work hours, or loss of coverage as the dependent of an employee receiving coverage.

While COBRA plans sound like an easy choice, keep in mind that they can be pricey. Without the contribution from your employer, paying 100% of premiums (plus a small administrative fee) may be unaffordable.

ACA Plans

The Affordable Care Act is a U.S. health reform law that offers subsidized government health care for American households with incomes between 100% and 400% of the federal poverty level. Open enrollment runs from November to mid-January, but you may receive ACA coverage with a qualifying life event.

Because ACA plans are subsidized to make healthcare affordable, they’re a much more budget-friendly option than other plans. However, ACA, sometimes called Obamacare, isn’t strictly temporary, like short-term health insurance, so if you only need coverage for something like a trip, consider other plans upfront.

Under the ACA, being denied coverage for a pre-existing health problem is prohibited, many screenings and preventive care services are covered, and generally, copays and deductibles are low, as the point of the law was to make health insurance accessible to those who couldn’t afford it previously.

International and Local Temporary Health Insurance Coverage

Short-Term Plans

Crafted for transitional care, short-term health insurance offers coverage for as short as a month and up to a year, with options of renewal. For immediate, flexible, affordable care, it fills the gap well. However, because short-term health insurance is not comprehensive, it may not cover all care.

Explaining Short-Term Health Insurance

Short-term health insurance is perfect for individuals who need coverage quickly while they are in between plans. You should consider short-term insurance if you:

- Are between jobs

- Are newly employed and waiting for benefits to begin

- Are a U.S. resident who has retired and is waiting for Medicare to start

- Are a U.S. resident who is waiting for ACA to kick in

- Are a U.S. resident who missed the enrollment deadline for ACA

- Just turned 26

- Just graduated college

- Plan to travel for more than a month or two

Not all short-term health insurance plans are created equal, so some companies and plans will cover many of these services while others will not. You can also purchase international short-term health insurance, which can grant you access to a worldwide network of providers.

If you don’t have many health needs, opting for a less-comprehensive plan could save you a chunk of money, but if you need your temporary coverage to check more boxes of care, the extra dollars are well worth the money to keep you safe.

How to Qualify for Short-Term Health Insurance

Most individuals will qualify for short-term health insurance. Many companies will ask you to complete a short questionnaire that outlines your health history and information on how you have used policies in the past.

If you meet a company’s screening requirements, you’ll likely have coverage within a couple days. Private insurance companies usually require this cursory medical underwriting in order to gauge the risk of insuring an individual and so assess the best plan for that individual.

Some plans may not approve you if you have pre-existing conditions such as cancer or pregnancy, if you are a man weighing more than 300 pounds or a woman weighing more than 250 pounds, if you qualify for other insurance such as Medicaid, or you are not a U.S. citizen.

Those with more complicated health needs will likely deal out higher payments while those with better health or fewer medical needs will find lower prices.

What Short-Term Health Insurance Covers

Most short-term health insurance covers preventative care, emergency care, urgent care, and medical test, with some plans also offering discounts for prescription medications, but each plan’s coverage will depend on which plan you choose.

Most short-term insurance does not often cover pre-existing conditions, mental health services, maternity care, and substance abuse.

What to Consider When Buying Short-Term Health Insurance

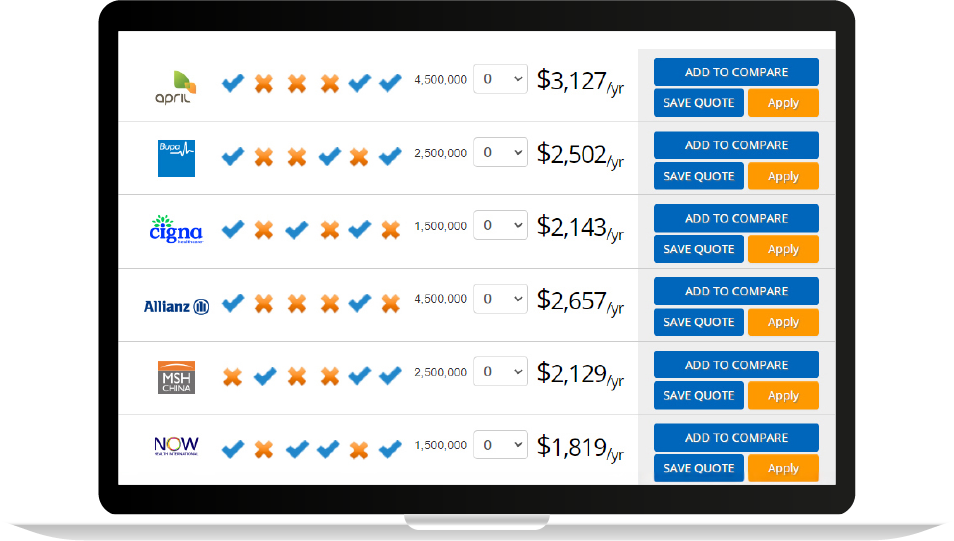

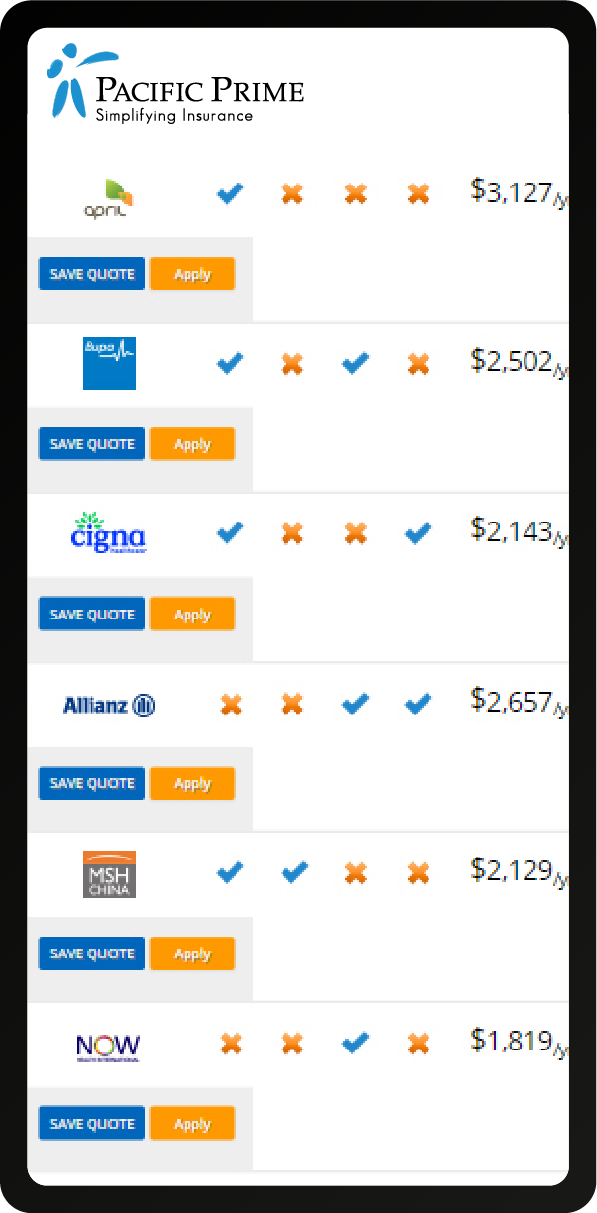

Pacific Prime partners with top-notch companies with globally renowned networks to provide the best short-term health insurance, specializing in short-term insurance for travelers and expats living overseas. Check out our site and find a plan that fits your needs, and keep these in mind:

Premium

Your premium is the monthly cost you pay to have insurance. Your premium cost will depend on how many people need coverage, their health history, deductible and out-of-pocket costs, and breadth of coverage.

Copay

The copay cost is the amount you pay when you finish a service, such as a doctor’s visit. Copay costs usually go toward your deductible and out-of-pocket maximum.

Deductible and Out-of-Pocket Maximum

A deductible is the amount you pay before your insurance pays for covered expenses. In contrast, your out-of-pocket maximum is the highest total amount you pay for medical services within a twelve-month period. Keep in mind that not all short-term health insurance plans have out-of-pocket maximums.

Personalized Needs

It goes without saying, but beyond costs, covering your specific needs should be at the top of your priority list, whether that includes finding drug coverage for pricey prescriptions, or opting for a lengthier plan as you look for new employment.

In looking for a new plan, many filter their plan options to remain with specific doctors who specialize in treating their condition—or who they’re simply most comfortable visiting. Insurance companies make it easy to find highly rated doctors and caregivers in network, but not all offices take all insurances.

If you have already established care with a doctor, some will accept a change of insurance. However, if remaining at the same doctor’s office or with specific medical professionals is important to you, call the office and clarify their insurance policies first.

Frequently Asked Questions

What is temporary insurance coverage referred to as?

Temporary health insurance is usually called short-term health insurance.

What insurance is considered temporary coverage?

Enrollment plans vary in length, but short-term insurance is considered temporary, with some plans as brief as a month while others may span a year, with renewal options. Some states limit short-term insurance availability to three months.

Can I obtain temporary health insurance in the USA?

All states except Hawaii, Washington, California, Colorado, New Mexico, Minnesota, D.C., New York, New Jersey, Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, and Maine allow temporary health insurance. Oregon, Delaware and Maryland restrict short-term plans to three months.

How can I obtain health insurance in the USA if I don’t have a job?

See if you qualify for Medicaid, CHIP, or an ACA subsidized plan. You may also be able to join a partner’s health insurance plan. If you recently left your employment, you may extend your health insurance using a COBRA plan.

What type of insurance coverage starts right away?

Most short-term health insurance plans start right away, even the day after you apply. Because short-term health insurance is customizable, you can choose when you would like your coverage to begin and to end.

How do I cancel my short-term health insurance?

When you apply, indicate start and end dates for coverage. Once your chosen end date has passed, coverage ends automatically. If you need to end coverage early, call the customer support number on the back of your insurance card. You may be asked to fill out a form or provide written confirmation.

What questions will I need to answer on my health insurance questionnaire?

Questionnaires ask for your medical history such as substance use, consultations or treatments, diseases or impairments and what medications you may take, and information on hospitalizations or overnight stays you may have had in the last five years. They also include policy-use-related queries.

Conclusion

Whether you elect to keep coverage from your previous employer through a COBRA plan, you stick with an ACA plan, or you pick short-term health insurance for an extended stay in Hong Kong, don’t let finding the right plan give you need for a mental health day.

Pacific Prime makes it easy to get a quote, so visit our page on short-term health insurance, or check out this article on flexible short-term insurance to research more about specific plans.

Serena earned her Bachelor’s Degree in Psychology from the University of British Columbia, Canada. As such, she is an avid advocate of mental health and is fascinated by all things psychology (especially if it’s cognitive psychology!).

Her previous work experience includes teaching toddlers to read, writing for a travel/wellness online magazine, and then a business news blog. These combined experiences give her the skills and insights she needs to explain complex ideas in a succinct way. Being the daughter of an immigrant and a traveler herself, she is passionate about educating expats and digital nomads on travel and international health insurance.

- How to Compare Travel Insurance Plans the Smart Way – October 21, 2025

- Best Hospitals in the UAE: Top Picks in Dubai and Abu Dhabi – October 21, 2025

- How Much is a Doctor Visit in Dubai Without Insurance? – October 21, 2025