300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

While not mandatory for immigration, obtaining health insurance is strongly advised for individuals of all ages and backgrounds in the US. When relocating to the US, foreigners and immigrants may encounter numerous unfamiliar challenges, and health insurance can often be overlooked.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Moving to a new country introduces unforeseen stressors and risks, and securing sufficient health coverage is crucial to avoiding substantial medical expenses.

Whether you seek basic protection or comprehensive care, various options exist to safeguard yourself and your loved ones in the US. This guide assists you in discovering optimal health insurance solutions for foreigners in the USA.

Health Insurance for Expats in the USA

Health insurance in the USA is generally not mandated by the federal government, and this holds true for expats and US citizens. Despite this, due to the exorbitant healthcare expenses in the US, it is highly advisable to secure coverage to prevent potential financial strain.

Although not obligatory, obtaining US medical insurance is strongly encouraged to mitigate hospital costs and ensure access to appropriate medical services. Moreover, as noted below, there are exceptions to the general rule that health insurance is not mandatory in the US.

The necessity for healthcare coverage in the US varies based on your nationality and visa category. Certain visas may necessitate at least basic insurance. Given the notably high medical expenses in the US compared to global averages, forgoing health insurance is ill-advised.

The US experiences high medical inflation rates, and often requires extensive testing before treatment, leading to increased expenses. Cutting-edge medical facilities and superior client service further contribute to these elevated costs.

What Type of Health Insurance Should I Secure?

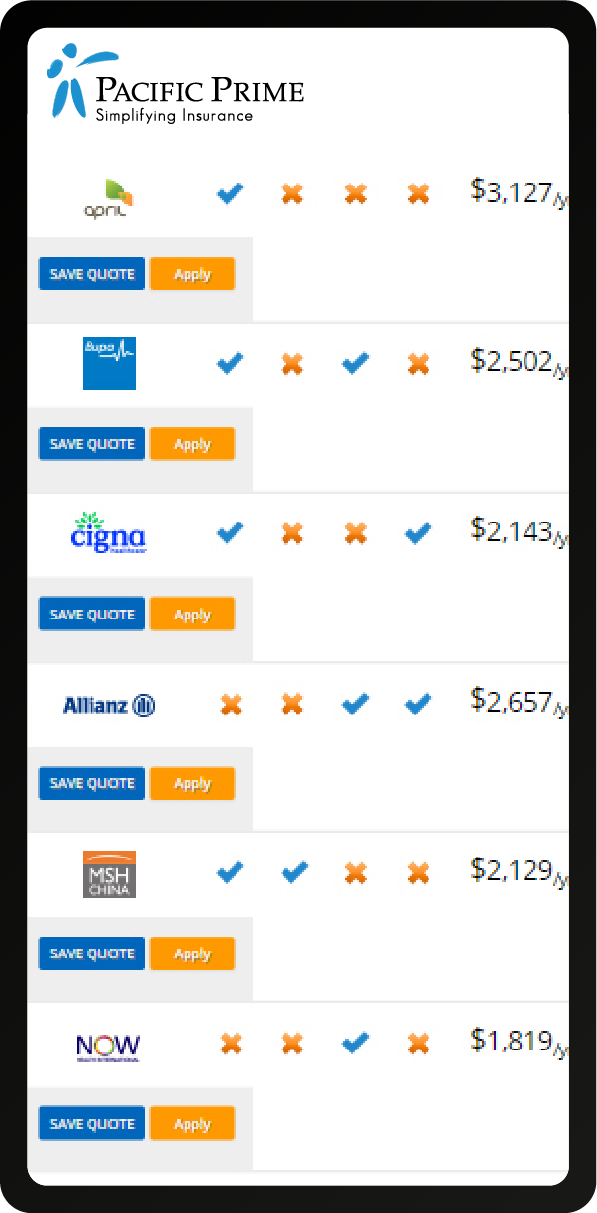

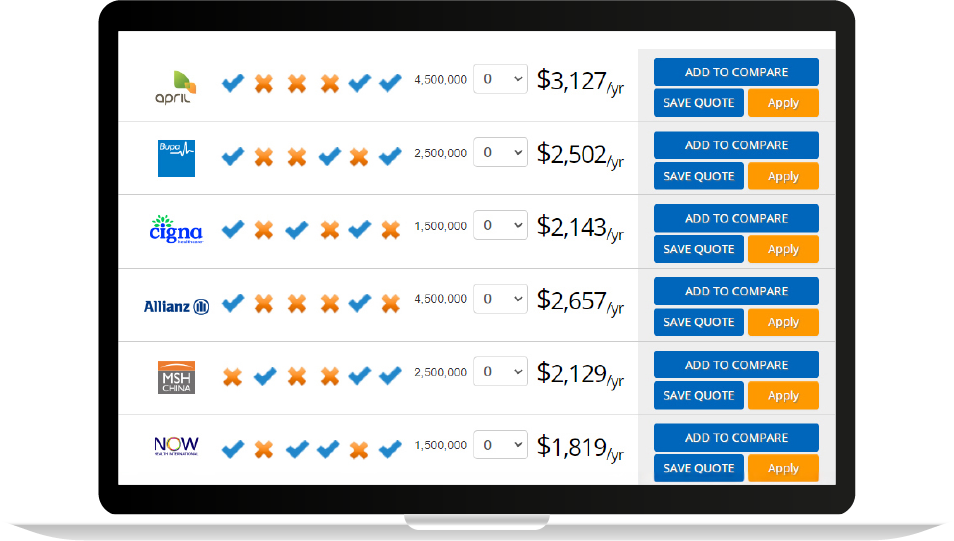

These are the international insurers that we recommend.

Health Insurance for Non-US Citizens, Foreigners, Including Immigrants

Health insurance for non-US citizens, foreigners, and immigrants is essential in the US, where healthcare is predominantly privatized, leaving public healthcare accessible to only a limited population segment. Consequently, the majority, including locals, rely on private health insurance.

Federal healthcare programs like Medicare cater exclusively to retirees, while Medicaid serves the country’s economically disadvantaged individuals. As a new immigrant seeking health coverage, you won’t qualify for either program.

Upon employment in the States, employers typically offer coverage that extends to immediate family members. However, this coverage often falls short of meeting the considerable expenses associated with doctor visits, medications, emergency care, and hospital stays.

In such cases, opting for an international health plan is often the most suitable choice for non-US citizens, providing access to diverse medical treatments globally.

Health Insurance for New Immigrants

While health coverage isn’t obligatory for many foreign nationals applying for an immigration visa, this regulation has recently undergone revisions and may do so again. Certain visas, such as the J-1, mandate documentation of coverage from an authorized provider.

For the latest details about the prerequisites of your specific visa category, refer to the J1 Visa Insurance Requirements.

Health Insurance for Foreign Nationals in the USA and ACA Penalties

Under the Affordable Care Act (ACA), also known as Obamacare, the shared responsibility provision, commonly termed the individual mandate, aims to ensure that all US citizens and permanent residents have access to high-quality and affordable health coverage.

To finance this initiative, the government mandates that most individuals acquire a minimum level of coverage.

The individual shared responsibility provision applies to all US residents, encompassing permanent residents and foreign nationals meeting the criteria to be classified as resident noncitizens for tax purposes after a specific period in the US.

This group includes non-resident noncitizens who fulfill specific presence conditions and opt to be treated as resident noncitizens.

Non-residents, including international students holding F, J, M, and Q visas, are exempt from the individual mandate during the initial 5 years of their US residence.

Regarding individuals in the J category, such as teachers, trainees, au pairs, students, and travelers, the ACA stipulates a 2-year exemption from the individual mandate.

Starting from the 2019 plan year (about taxes filed in April 2020), the ACA’s Shared Responsibility Payment is no longer in effect. Consequently, individuals who do not fulfill the criteria of the individual mandate are no longer obligated to pay a penalty going forward.

Exemptions from the Individual Mandate

Foreign nationals residing in the US for a duration short enough to avoid meeting the criteria for being classified as resident noncitizens for federal income tax purposes are excused from the individual mandate.

For further clarification on when a foreign individual qualifies as a resident noncitizen for federal income tax purposes, refer to the IRS website.

Individuals eligible for exemption under this regulation include:

- Non-resident noncitizen

- Dual-status noncitizen in their initial year of US residency

- Non-resident noncitizen or dual-status noncitizen opting to file a joint return with a US spouse

- Those submitting a Form 1040NR or Form 1040NR-EZ, comprising a dual-status tax return for their final year residing in the US as a resident

- Individuals meeting the criteria for a personal exemption on Form 1040NR or Form 1040NR-EZ

Healthcare Insurance for Visitors in the USA

If your stay in the US is anticipated to be under a year, opting for a travel medical plan might suffice to meet your healthcare requirements. This strategy is especially advantageous for younger travelers seeking basic emergency protection.

Before you arrive in the country, it’s crucial to determine whether you require travel insurance for the USA. Verify whether the policy should originate from your home nation, the US, or a combination of both.

Typically, travel plans offer coverage for accidents and illnesses, alleviating the burden of substantial medical costs linked to doctor consultations and hospitalizations. Additionally, such policies grant access to pharmaceutical services and translation assistance, should the need arise.

For non-citizens, immigrants, or international travelers, we recommend considering a global medical plan. Our resources provide guidance to aid in selecting an international health insurance plan tailored to your specific requirements.

Health Insurance Costs in the USA

Diverse options exist within global medical plans. Opting for cost-effective catastrophic coverage, which primarily addresses severe scenarios, proves beneficial for budget-conscious travelers.

Conversely, comprehensive medical plans encompass a broader spectrum, potentially covering physician consultations, hospital stays, prescription medications, laboratory services, and chronic disease management.

Our most economical global medical plan falls within the range of USD $400 to $500 annually, while the most extensive but priciest options can reach up to USD $30,000 to $40,000 per year.

Short-term travel medical plans commence at approximately USD $1.50 daily, with costs varying for older customers or for those seeking more comprehensive coverage, potentially exceeding USD $10 per day.

Deciding How Much Coverage You Will Need for Health Insurance in the USA

To answer this question, there are a few issues you need to first consider.

The Typical Expenses for Medical Services at Healthcare Facilities or Hospitals in the US

This question proves challenging due to the atypical nature of healthcare costs in the US. However, one undeniable fact is that these costs rank among the highest globally. Opting to pay for healthcare expenses out of pocket in the United States can swiftly deplete your financial resources.

Under a medical insurance plan, the average copay for a doctor’s visit within your network ranges from USD $15 to $25. Specialist consultations typically incur higher fees.

Moreover, many plans entail copays for urgent care, emergency visits (approximately USD $250), and prescription medications. Without insurance coverage, these expenses can skyrocket, often reaching 10 to 100 times the cost.

Healthcare expenditures also fluctuate based on the ailment, medical procedure, and healthcare facility. While comparing costs for various procedures within the same facility is straightforward, expenses such as an appendectomy can significantly escalate.

This is so especially if the procedure is performed at a hospital that does not accept your insurance plan. It is therefore crucial to exercise caution when selecting your plan and conduct thorough research on nearby hospitals to ensure coverage.

Removing Benefits That Are Unnecessary to Reduce the Cost of Your Plan

Depending on your chosen plan, it is possible to reduce costs by excluding unnecessary benefits. By collaborating closely with a reputable insurance broker, you can tailor a plan that aligns with your specific healthcare requirements and financial constraints.

For instance, if you are a young, healthy individual without dependents or preexisting conditions, you may consider minimal coverage — sufficient to safeguard you from overwhelming medical expenses in scenarios like accidents or severe illnesses.

Even if you are older, have family members requiring coverage, manage a health condition, or encompass all these factors, comprehensive coverage might not be imperative for your safety.

Our team can assist you in devising a plan that addresses your essential needs without imposing unnecessary charges. So contact us today!

Determining How Much Insurance You Should Purchase

Selecting a US health insurance policy involves various considerations. Here are key factors to keep in mind:

- Duration of your stay in the country

- Nature of your work as an expat

- Presence of any underlying medical conditions

- Willingness to pay beyond the maximum coverage limit when necessary

- Monthly budget allocation for coverage

Additionally, assess the feasibility of returning home for additional services if required, especially in cases of serious medical conditions necessitating repatriation in emergencies.

For short stays in the US, such as a few months to a year, with existing coverage in your home country, you might consider opting for a lower maximum coverage amount.

Your employment terms may dictate a minimum tenure, during which time you may potentially require medical treatment within the US. This would affect your insurance costs with a potentially higher maximum coverage amount.

Potential Consequences of Living Without Health Insurance in the US

Prior to deciding whether to self-pay for medical bills, it’s crucial to evaluate factors like proximity, accessibility, and the quality of healthcare providers at local medical facilities. Prices for identical procedures can significantly vary between different establishments.

It’s essential to remember that healthcare expenses are exorbitant, often leading to financial ruin for US residents.

Even if you lead a healthy lifestyle, unforeseen accidents or illnesses can still occur. While it might seem unjustified to invest in protection against unlikely events, particularly for those who are young and healthy, having coverage becomes invaluable when unexpected crises arise.

Allocating a small additional amount each month for insurance can prevent substantial expenses later on. For your well-being, peace of mind, and financial security, health insurance for non-residents in the USA is not to be skipped.

Costs of Accident and Emergency Care in the USA

Frequently, individuals reaching out to us inquire about the potential costs associated with an emergency room visit. Upon providing them with the current average figures, they are typically taken aback by the amounts quoted.

As per research conducted by the National Institute for Health, the typical price range for an ER visit fell between USD $290 and $690 depending on the patient’s age in 2017.

However, this figure can vary significantly based on the nature of the medical emergency you encounter, potentially resulting in costs higher or lower than this estimate.

The diverse pricing structures across different hospitals and clinics exacerbate fluctuations in charges based on the specific illness. Such wide-ranging cost disparities can come as a surprise if you are diagnosed with a medical condition.

One of the primary advantages of possessing an international health plan is its potential to offer cost-effective coverage — often providing superior healthcare services at more affordable rates.

Treatment from your physician at their practice or clinic typically incurs expenses that are 3 to 4 times lower than receiving the same care at a hospital from the same practitioner without any medical insurance coverage.

How Much Insurance Coverage Foreign Nationals Should Buy

Determining the appropriate level of health insurance coverage as a foreign national in the US is a personal decision influenced by factors such as your current health status, occupation, and length of stay.

Take into account these considerations along with other factors discussed in this piece to pinpoint the most cost-effective medical insurance option for your needs.

Policy maximums typically range from USD $50,000 to $5 million per period, usually on a per-person basis. Some plans offer unlimited coverage.

To simplify the process of selecting suitable health coverage, adhere to this guideline:

- For a 5-day to 1-month stay, consider USD $50,000 to $100,000 in medical coverage.

- For stays lasting 1 to 3 months, opt for coverage ranging from USD $100,000 to $500,000.

- For stays exceeding 3 months but less than a year, seek a policy with a minimum coverage of USD $250,000.

- For stays of a year or longer, secure at least USD $1 million in annual coverage. Increase coverage if your family will be residing with you, especially if all of you intend to receive treatment in the US. In cases where critical illnesses are a concern or for extended stays in the US, opt for plans offering unlimited coverage.

Elderly individuals and those traveling with a larger group to the US face elevated claim risks, warranting full-coverage health insurance plans with higher limits and comprehensive coverage.

Selecting the Right International Plan

Ensure you choose the right type of policy. For short-term travels spanning one to two years, a travel medical plan is recommended. For extended stays extending over multiple years, an international health insurance plan proves to be a more suitable choice.

Get your FREE no-obligation quote for short-term travel medical insurance (covers emergency medical issues along with other travel benefits) or long-term global medical insurance (comprehensive medical coverage with annual renewal) today!

Pre-existing Medical Conditions and Health Insurance in the US for Foreigners

In the US, health insurance coverage for individuals with pre-existing medical conditions has undergone significant improvements and protections with the implementation of the Affordable Care Act (ACA).

For foreigners residing in the US, understanding how these regulations impact their healthcare options is crucial.

The Affordable Care Act (ACA) and Pre-existing Conditions

The ACA, signed into law in 2010, brought about substantial changes in how health insurance companies handle pre-existing conditions. Here are key points to consider:

- Coverage Mandate: Under the ACA, all Health Insurance Marketplace plans are required to cover treatment for pre-existing medical conditions. This means:

- No plan can reject you, charge you more, or refuse to pay for essential health benefits due to a pre-existing condition.

- Once enrolled, coverage cannot be denied or rates increased based solely on health status.

- Medicaid and CHIP also cannot deny coverage or apply higher charges due to pre-existing conditions.

- Pregnancy Coverage: If pregnant at the time of application, insurance plans cannot reject or charge more because of pregnancy. Once enrolled, pregnancy and childbirth are covered from the plan’s start date.

- Special Enrollment Period: Giving birth or adopting a child qualifies for a Special Enrollment Period, allowing enrollment or plan changes outside the Open Enrollment Period.

Coverage Options for Foreigners

Foreigners in the US have various avenues to access health insurance coverage, including:

- Marketplace Plans: Foreigners can enroll in Marketplace plans that offer comprehensive coverage for pre-existing conditions. These plans provide essential health benefits and preventive services.

- Grandfathered Plans: Some older health insurance plans (grandfathered plans) may not cover pre-existing conditions. Foreigners with such plans have options:

- Switch to a Marketplace plan during Open Enrollment.

- Purchase a Marketplace plan outside Open Enrollment when the grandfathered plan year ends.

Further Considerations

- Special Enrollment: Certain life events, such as moving, marriage, or adoption, can trigger a Special Enrollment Period, allowing individuals to enroll in or change health plans.

- Resources for Assistance: HealthCare.gov provides tools to estimate income, find local help, submit documents, and appeal decisions, assisting foreigners in navigating the healthcare system.

- Language Support: HealthCare.gov offers information in multiple languages, ensuring language barriers do not hinder access to vital healthcare information.

How to Choose the Right Health Insurance Copayment and Deductibles for Foreigners in the US

When navigating the complex landscape of health insurance in the US as a foreigner, understanding the nuances of copayments and deductibles is crucial. These financial elements not only affect your out-of-pocket expenses but also play a significant role in determining your overall healthcare costs.

Understanding Copayments and Deductibles

Copayments and deductibles are key components of health insurance plans that can impact your premiums and the amount you pay for healthcare services. Here’s a brief overview of how they work:

Copayments (Co-pays)

A copayment is:

- A fixed percentage or amount paid by the insured for covered medical services.

- Usually applied per visit or service.

- Can vary based on the type of service, such as standard doctor visits, specialist consultations, or emergency room visits.

Deductibles

A deductible is:

- A fixed amount must be paid by the insured before the insurance company starts covering costs.

- After meeting the deductible, beneficiaries often pay a percentage of costs (co-insurance) until reaching their out-of-pocket maximum for the year.

Using Copayments and Deductibles to Control Premiums

Opting for higher copayments and deductibles can lead to lower monthly premiums. This strategy can be beneficial for those who don’t anticipate frequent medical visits or have the financial capacity to cover higher out-of-pocket costs when needed.

While higher copayments and deductibles can help reduce premiums, being too aggressive with these cost-sharing features can have drawbacks.

Risks of Aggressive Copayment and Deductible Strategies

Choosing excessively high copayments and deductibles to lower premiums could result in unexpected financial burdens during medical emergencies or when facing significant healthcare costs.

High copayments might discourage individuals from seeking necessary medical care, potentially leading to untreated health issues and more significant costs down the road.

Tips for Choosing the Right Copayments and Deductibles

To ensure you make the right choices regarding copayments and deductibles, we urge you to:

Assess Your Healthcare Needs

Consider your health status, medical history, and anticipated healthcare needs to determine the level of coverage that suits you best.

Budget Considerations

Balance your monthly budget with potential out-of-pocket costs to ensure you can comfortably afford copayments and deductibles.

Comparative Analysis

Compare different plans to understand how copayments, deductibles, and premiums interact to find the optimal balance for your situation.

Seek Professional Advice

Consult with insurance representatives or healthcare professionals to gain insights into the implications of different copayment and deductible levels.

Reasons Why Foreigners in the US Should Consider Medical Evacuation Insurance

Foreign nationals residing in the United States may find themselves in situations where having medical evacuation insurance can be crucial. Despite the advanced healthcare facilities in the US, unforeseen circumstances can arise where medical evacuation becomes necessary for foreigners.

Here are compelling reasons why foreigners in the US should consider investing in medical evacuation insurance:

Geographical Considerations

The vastness of the United States can result in individuals residing in remote areas where access to specialized medical care might be limited. In cases of serious illness or injury, especially in rural regions, timely evacuation to a more equipped medical facility may be essential.

Financial Protection

Medical evacuation costs can be exorbitant, especially if air transport or long-distance travel is involved. Having insurance coverage for medical evacuation ensures that foreigners do not have to bear the steep expenses associated with such emergency services.

Comprehensive Healthcare

While the US offers high-quality healthcare services, certain specialized treatments or facilities may not be available locally. Medical evacuation insurance guarantees access to a broader range of medical facilities, ensuring the best possible care in critical situations.

Travel and Exploration

For foreigners who enjoy traveling within the US, having medical evacuation insurance provides peace of mind while exploring diverse regions. Emergency evacuation coverage eliminates concerns about medical emergencies disrupting travel plans or causing financial strain.

Natural Disasters and Emergencies

In the event of natural disasters, such as hurricanes or wildfires, medical evacuation insurance can facilitate swift relocation to safer areas. This coverage ensures prompt evacuation in emergency situations where local healthcare services may be overwhelmed or inaccessible.

Family Support

Medical evacuation insurance can also include provisions for family members to accompany the individual during evacuation, fostering emotional support during challenging times. The assurance of having loved ones nearby can significantly aid in the recovery process.

Peace of Mind

Ultimately, having medical evacuation insurance offers foreigners in the US peace of mind, including expats, knowing that they are prepared for unexpected medical emergencies. It provides a safety net that mitigates the stress and uncertainty associated with unforeseen health crises.

Frequently Asked Questions

Do foreigners moving to the US need health insurance?

Health insurance isn’t mandatory for immigrants, but it’s highly recommended due to costly medical services in the US.

Is the Affordable Care Act applicable to all foreigners in the US?

Foreign nationals, including expatriates and non-residents, are generally not subject to the ACA’s individual mandate.

What health insurance options are available for short-term visitors to the US?

Travel medical plans are suitable for short-term stays, providing coverage for emergencies, doctor visits, and hospitalization during the visit.

Conclusion

The assurance of medical benefits offers a sense of security, ensuring coverage for potential illnesses or emergencies.

While the peace of mind that accompanies having medical insurance in the USA comes at a cost, the expense of a health policy typically proves more affordable than bearing hospital expenses independently.

To facilitate your decision-making process regarding the most suitable policy, review our list of leading international health insurance firms, carefully assessing the advantages and limitations of each provider.

Pacific Prime remains on hand to assist you. With 20+ years of experience in international health, expat health, travel, and many more categories of insurance, our ability to tailor the exact right plan for your needs and budget is unsurpassed.

What’s more, you can rest assured the plans we recommend will offer the best value for your money, and our advice and support are free to you because you won’t be paying more than securing your coverage directly from an insurer!

So, contact us today!

Are you visiting South Africa or the UK soon? If so, our articles on the best hospitals in South Africa for expats and visitors and the best hospitals in the UK for expats and travelers are must-reads for you.

Since joining Pacific Prime, Martin has become even more aware of the gap between the true value of insurance products and most people’s appreciation of it, and developed a passion for demystifying and simplifying matters, so that more people get the protection they need at a cost they can easily afford.

In his free time, Martin attends concerts of various genres, and plays the violin with piano accompaniment he pre-recorded himself or played live by his niece.

- Bali Visa on Arrival: Essential Guide for Travelers – October 17, 2025

- Cost of Living in Costa Rica: Expat Guide – October 15, 2025

- Top 11 Insurance Companies in Curaçao for Expats – October 8, 2025